What are the architecturally-significant use-cases for identity?

Some of the most interesting uses for cryptocurrency technology in finance are securities processing, supply chain finance and derivatives operations. These are areas where there should be almost total automation but there is, in reality, still large amounts of manual processing, rework, reconciliation, complexity and endless opportunity for confusion and dispute.

To help think about how blockchain technology could play a role, I suggested the “trust bundles” concept as a way to think about which aspects of a given business, such as securities exchange and settlement, could be moved onto a decentralized consensus system – and what benefits might accrue.

However, there’s a big problem that needs to be addressed before many of these opportunities become realistic. That problem is identity. The anonymity (or pseudonymity) of Bitcoin may be great for some use-cases but it doesn’t help a firm accused of paying a “crypto dividend” to a terrorist if they have no way of proving they didn’t!

So let’s imagine we’re living in the future… Smart property technology means that securities can be issued and traded on a blockchain-like system and smart contract technology has allowed us to move all derivatives contracts onto a global platform.

What identity problems would we need to have solved for that future to come true?

Smart Property Issuance

Imagine you’re an investor. You have a Smart Property wallet. Perhaps it contains multiple cryptocurrencies, some bank-issued fiat currencies and your equity portfolio, safely secured with a multi-signature scheme.

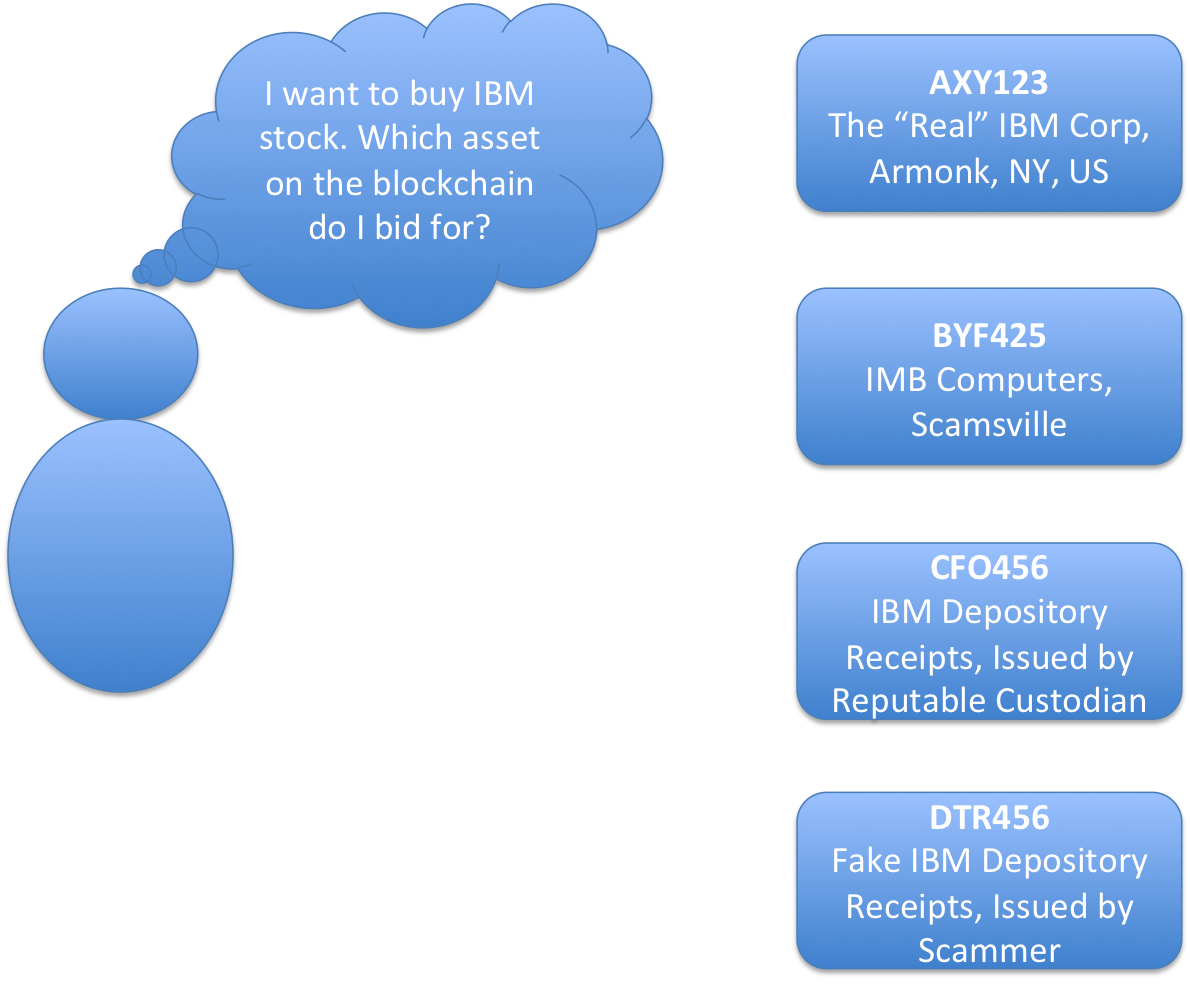

You decide you want to add some IBM stock to your portfolio. So you instruct your wallet to place an order on a decentralized equities exchange.

What do you place the order for?

What do you physically type into the user-interface to tell it you want IBM stock and not somebody else’s stock?

It would be nice if you could simply type “IBM”.

But how would that work? We’re in a decentralized world, remember. We’ve “unbundled trust”. So how should the wallet interpret “IBM”? Which asset on the decentralized ledger represents the “real” IBM? A Namecoin-like system doesn’t help if a “cryptosquatter” took the IBM name before the real IBM did.

And, in any case, what do you mean by “IBM”?

Intuitively, you probably mean something like: “The big American IT company based in Armonk, New York that had 2014 revenues of about $100bn and is a component of the Dow”. Or something like that. But how to capture that intuition in a way that a decentralized network can interpret?

And how to distinguish the security you want from something similar (and legitimate) issued by somebody else? And, of course, how to distinguish it from a security issued by a fraudulent third party who is trying really hard to fool you into buying their product?

In a pseudonymous world, how do I distinguish “real” blockchain assets from scams?

One really unimaginative way would be to do what we do today: just decide to trust somebody to do the mapping for you. Tell your wallet that you trust Bloomberg or Markit, say, to maintain a directory and you’re done. This would be an oracle service, in effect.

But this is a new point of centralization. Whoever controls that list can extract a rent and they are a source of risk: what happens if their database gets hacked or a rogue employee changes the records? Maybe having multiple oracles is the way forward.

Alternatively, perhaps we can use the internet X.509 Certificate system as a model. But even that would require some thought: you don’t want your webmaster issuing a $1bn bond!

What does it mean to be an issuer?

But we also need to think about it from the perspective of the issuer and this is altogether more difficult. To keep things interesting, let’s use a currency example this time.

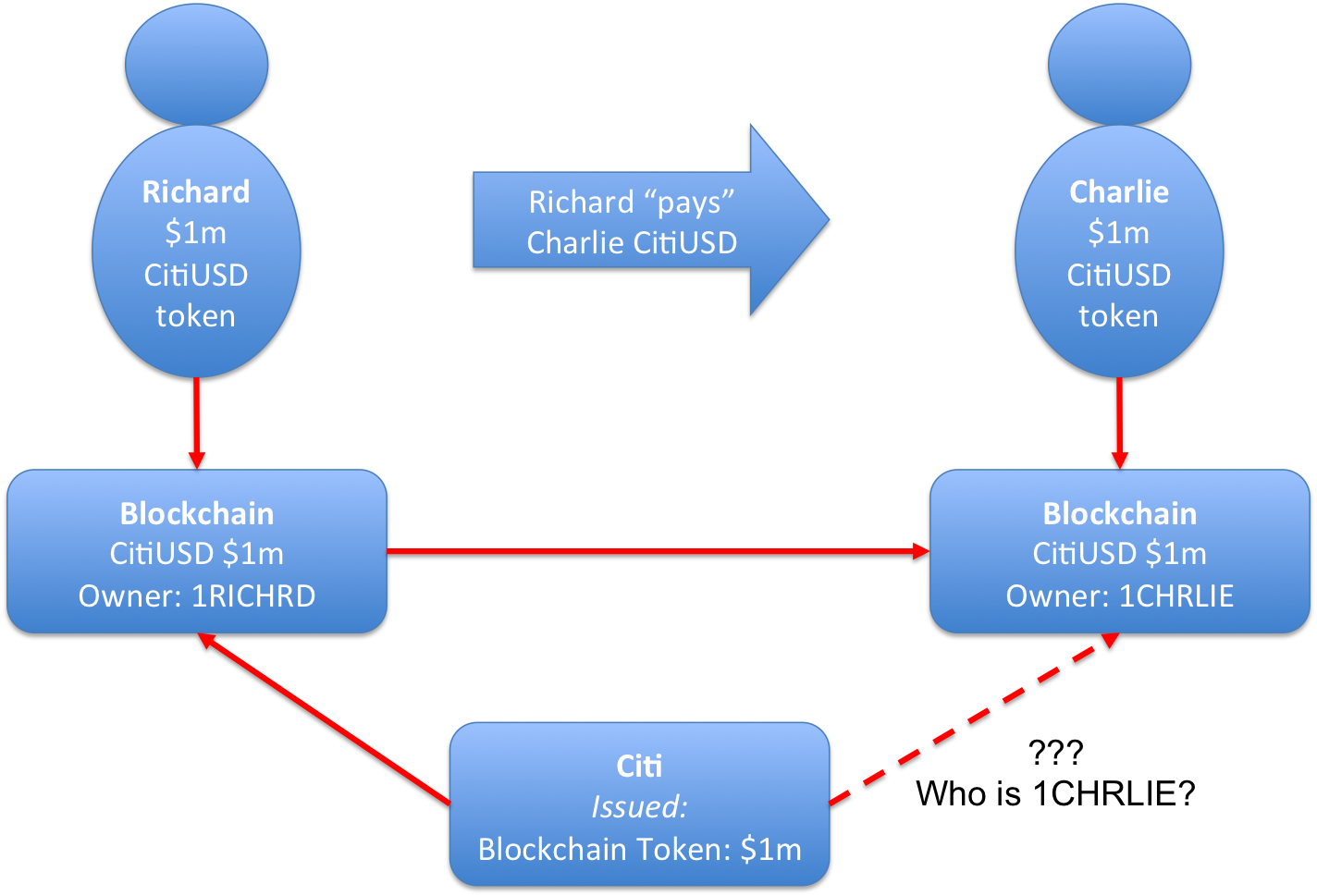

Imagine we’re still in the future and I am a customer of Citi with a $1M balance. I could ask Citi to issue a token on the blockchain representing this balance and send it to my wallet. My balance in my Citi account would be converted into ownership of a token representing $1M USD. (I shouldn’t need to state it but I will: I chose Citi purely as an example. I have no insight into their plans, if any, in this space!)

Richard is a Citi customer. Citi converts Richard’s balance into a “CitiUSD” token on a blockchain and sends it to Richard’s “1RICHRD” address

So I would now be a holder of a 1M CitiUSD token, owned by my “1RICHARD” address. Note that this is essentially what happens when I use a gateway on the Ripple system but let’s assume we’re on a blockchain system for now to keep things consistent.

Aside: imagine if all banks did this… we could have CitiUSD, ChaseUSD, BarclaysGBP all issued on the same platform. Perhaps they’d trade at different prices based on market perception of their credit-worthiness? Prices as a function of CDS spreads perhaps?

Now, Citi would know exactly who I was: I was already a customer, remember, and they needed to know my blockchain address to issue the token to me.

But think about what happens next. I now have full control of this token.

So I could send it to anybody else in the world. And that person would now own a token representing a claim of $1M against Citi. Let’s imagine I bought a house from Charlie and paid using my CitiUSD tokens, sending them to his blockchain address, 1CHRLIE

I “pay” Charlie with my CitiUSD tokens. So Charlie now owns the claim on Citi. But Citi had no part in this transaction…

What would Citi think about this? Who is “1CHRLIE”?? Are they already a customer? If not, how do they know if “1CHRLIE” is a “good guy” or not? Is Citi obliged to pay $1M upon presentation of the token?

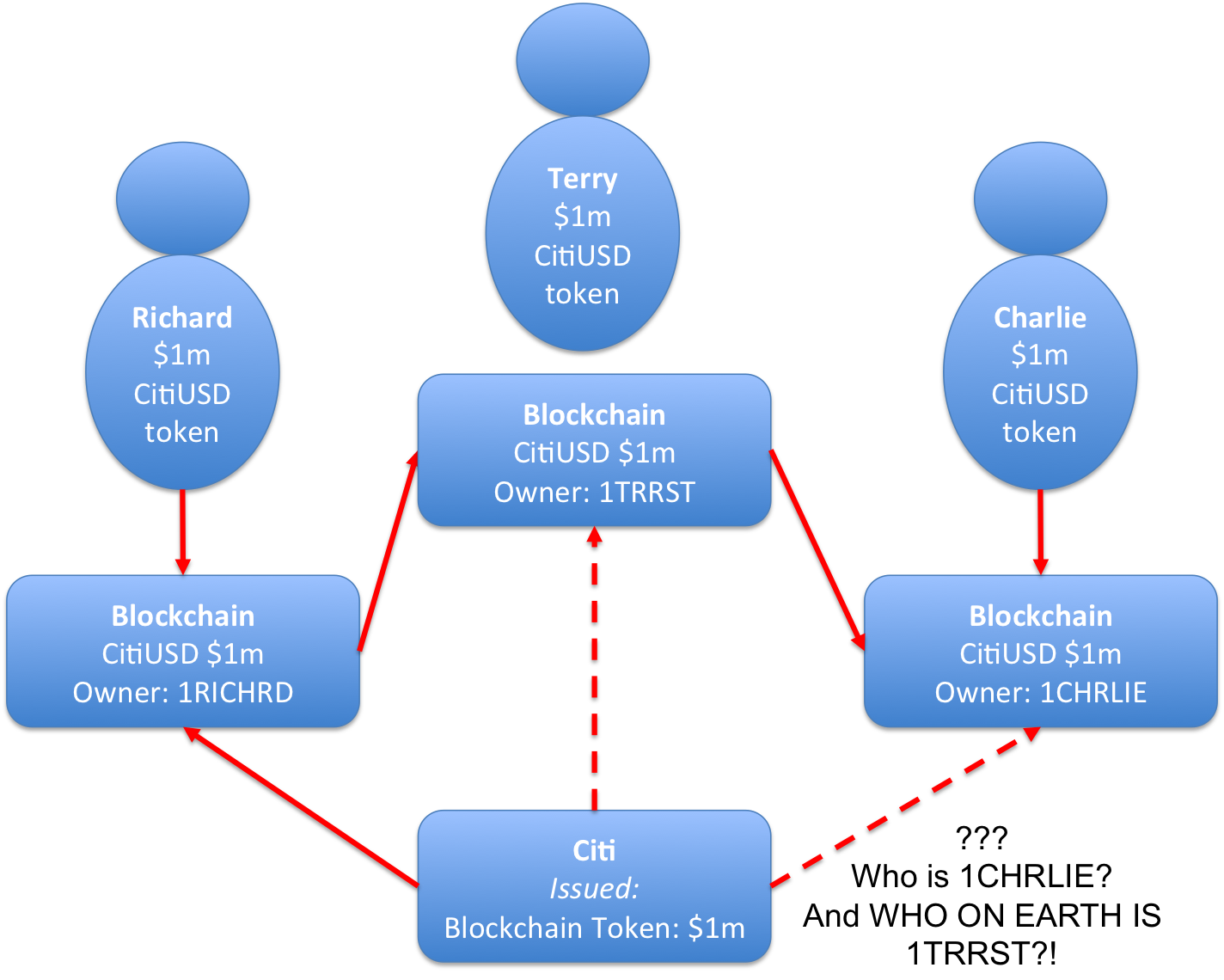

More trickily, what happens if the token has passed through the hands of a “bad guy” at some point between issuance and redemption? Sure – the initial owner of the token might be OK – and the person presenting the token some time later for redemption might also be OK. Perhaps we do know that 1CHRLIE is Charlie and that Charlie is a Chase customer and we’ve doubled checked with Chase. But do we need to know who has held the token in the intervening steps?

Do we need to know the identities of everybody who has ever owned a token?

What if one of the intermediate owners was 1TRRST, aka “Terry the Terrorist”?

You can be pretty sure we do need to know something about them. Good luck if you try to tell your regulator that these tokens are “bearer assets” that are morally equivalent to cash!

So, leaving aside the possibility that we just don’t go down this road at all, what are some of the options for making this work?

I think there are two broad options:

Option 1: Ex-Ante Prevention – The Issuing Bank “Co-Signs”

This option is pretty simple. You change the model so that these assets are not bearer assets. Holders of Citi tokens need to get Citi to co-sign any blockchain transactions that move the asset. So Citi gets the chance to vet the recipient and check they’re happy owing them money. You can think of this as “ex ante prevention”. It would work, of course, but it would heavily constrain the usefulness of such a system.

Option 2: Ex-Post Prevention – The Bank Won’t Pay Up Unless You’ve Behaved Yourself

This option is more interesting. You can send the token wherever you like, but if you want to redeem the token for real USD, the bank will ask you to prove that everybody who ever owned it was a “good guy”. If you can’t prove a clean ownership history then the token is worthless; the bank won’t pay up.

Leaving aside the question of what we mean by “good guy” and the natural worry that this could give banks an excuse to renege on their commitments, how might you do it?

First, let’s cover off the obvious option. The obvious option is simply to say: “We’ll only redeem a token if its ownership chain consists only of Citi customers”. Or perhaps you could extend it and say: “We’ll only redeem a token if its ownership chain consists of customers of the following banks”. The latter approach might pave the way for an industry “register” that maps bank identifiers to blockchain addresses. Again, we’re back to centralization and the very real risk of a “balkanization” of the system: you would effectively have “white” addresses and “black” addresses – those that can hold banking-system assets and those that cannot.

If several of my readers are about to explode in outrage, bear with me because this isn’t what I’m proposing…. Happily, there could be another way.

“Identity is the New Money”

I was fortunate last week to attend Consult Hyperion’s “Digital Identity” unconference at Barclays Bank’s “Escalator” venue in East London. Our host, Dave Birch, encouraged the audience to really exert themselves to think deeply about questions of digital identity. It gave me the motivation I needed finally to read his book, “Identity is the New Money”. I recommend it. It’s short, snappily written and made me think.

One of his key themes is that we’re thinking about identity all wrong. Most of the time we think we need to know who somebody is, what we actually need to know is something about them:

- A bartender doesn’t need to know your name; they just need proof you’re over 18.

- A UK doctor doesn’t need to know what town you were born in to know if you’re entitled to free healthcare.

- … and so on

Similarly, and at a very conceptual level(!), what an issuer of USD tokens on a blockchain needs to know is probably something like:

- The actor who controls an address is a legal person…

- … and this person has a US bank account…

- … and somebody has studied this person’s identification documents closely and has no concerns about them…

- … and whoever is making these statements about them is trusted by the issuer of the tokens (say Citi)

Now, I say “conceptual”, because AML, KYC and CDD regulators might not see things this way yet but let’s keep going…

What these concepts all have in common is that they have this idea of a “certifier” – somebody or something that:

- Is trusted by the issuer

- Ties something I have (my face or my blockchain address) to something I am (“over 18”, “a holder of a US bank account”, etc)

If you trust the certifier then you can trust that somebody proving ownership of the face or the address is over 18 and a holder of a US bank account, etc.

What does a bank need in order to be satisfied?

So now let’s return to our currency example. Remember the problem we’re trying to solve: If I am Citi, I want to be sure that anybody who has ever held one of my tokens is somebody I am allowed to transact with.

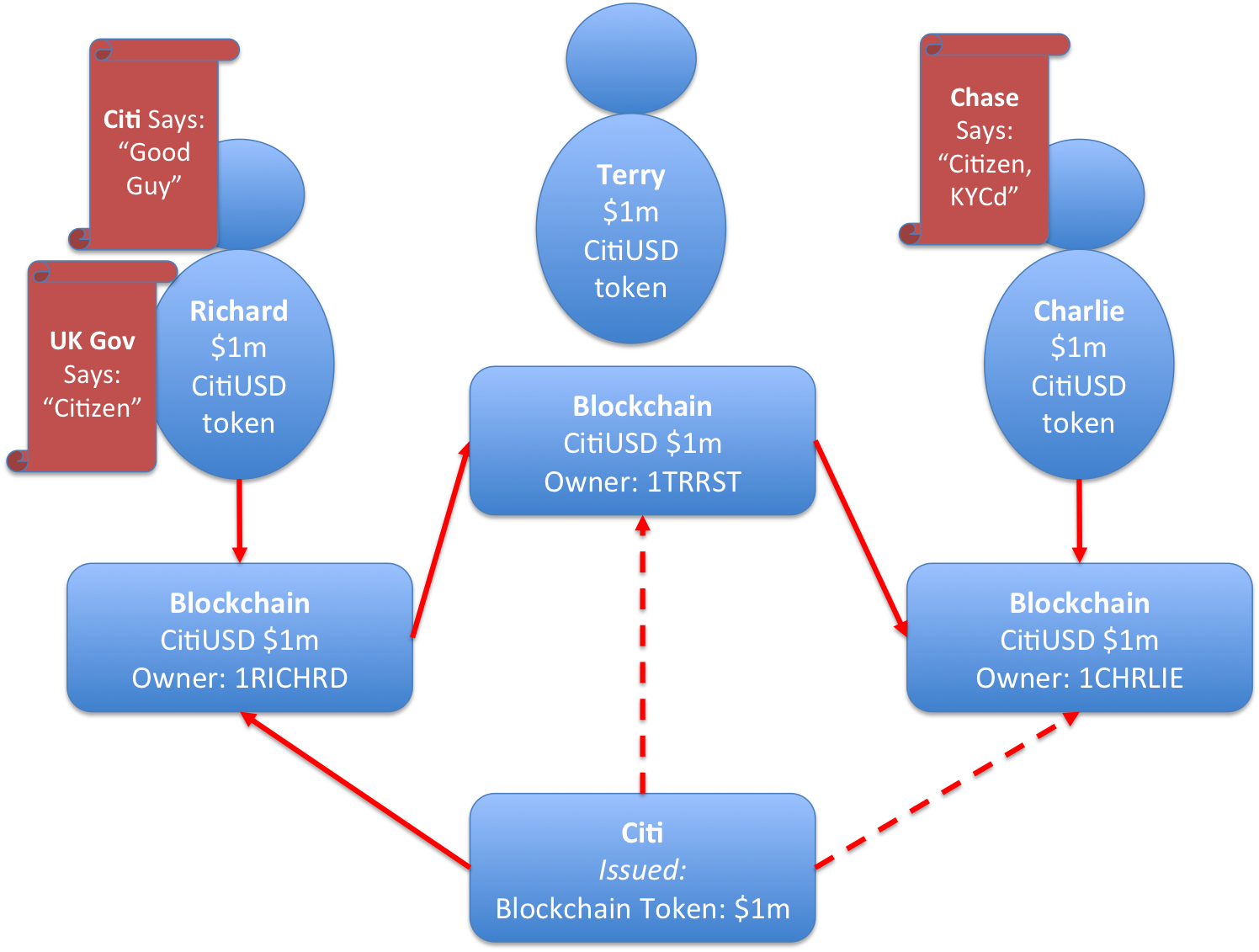

So how could we achieve this without a centralized database? Well, imagine Charlie is a customer of Chase.

- Let’s assume Chase knows who Charlie is and is satisfied that Charlie is a good guy.

- So if Charlie can prove to them that he controls a particular blockchain address, they might be willing to issue him with a “certificate”

- This certificate might say: “I am Chase. Here’s my proof. I know who is the owner of address 1CHRLIE…. That person is a US Citizen and, as of 3 December 2014 was a retail customer, with a good account history and no warning signs on his account”

And perhaps I could get a certificate from Citi that says they think I’m a “good egg” and one from the UK government confirming I’m a UK citizen:

Could asset issuers use certificates from third parties they trust to satisfy their regulatory and other “client due diligence” requirements?

So now we have something really interesting.

An issuer can set down their conditions when they issue the asset. They could say something like: “I will redeem this asset at par if the redeemer can prove that they and every intermediate owner was a US citizen with a KYCd US bank account. I will accept proof from any FDIC insured bank”.

So if I was considering buying a CitiUSD token from somebody, I no longer care who they are. I just care that they possess one or more certificates that comply with the conditions that were specified in the definition of the asset. My wallet software could even check it automatically for me.

And when somebody wants to redeem the token, they simply return it to Citi, with the chain of certificates and Citi can immediately tell that the token has only been in the hands of people with the attributes it specified. No need to reveal my identity to anybody and no central third parties we need to trust. If somebody does need to figure out the identity, they can get a court order and the certifier will reveal it.

Reality is more complex. In particular, how to stop a black market in certificates? e.g. a “mule” obtains a certificate for a blockchain address and then turns over the certificate and the address’s private key to a bad person. A difficult problem to solve but probably not unsurmountable.

But the underlying principle is absolutely crucial: if we’re moving to a world where trust is unbundled and control is decentralized, we need to rethink identity. Anchoring it in a diverse set of “certifiers”, who attest to the linkage between something I have (a blockchain address? My face?) and something I am (British, Over 18) surely has to be the way forward.

You seem to be dealing with a few issues here – security, bitcoin, and transactions. Maybe it would be easier to separate them out or maybe the point is to address the intersection. Non repudiation was addressed by encryption and PKI a while ago (eg http://security.stackexchange.com/questions/1786/how-to-achieve-non-repudiation). It’s funny that you say “you don’t want your webmaster issuing a $1bn bond”. In the 90s we were looking for trusted third parties to be the certificate authorities and it seemed like banks were the obvious answer. CAs do have different levels of security/assurance and should be able to go up to that level, although some have been compromised – the solution being to move to a federated model. Which I guess is what bitcoin gives you.

You lost me on the third paragraph. The burden of proof shouldn’t be on the accused to prove innocence. We should not focus on making bitcoin / blockchains conform to bad systems. We should focus on defunding those bad systems. The leverage is there in our favor. All that is needed is to make the lifeboat (bitcoin) easily accessible.

Here’s a great presentation on identity, issues with CAs, and the need for a federated model (skip the first 5 mins) https://www.youtube.com/watch?v=Z7Wl2FW2TcA

@samjgarforth – thanks for the comments, Sam. Agree: one of the arguments I was trying to make was that a federated model feels intuitively better suited to this world. But I was also saying something more: many of the scenarios today where actors have to reveal their identity are scenarios where the real requirement is something else: a need for the actor to prove possession of a particular attribute (age, nationality, whatever). Leaking identity information in order to prove possession of the attribute feels like a failure.

@ansel – “The burden of proof shouldn’t be on the accused to prove innocence”. Agreed but that is, unfortunately, a normative statement, Empirically, the reality is that many actors today live in a world where they *do* have to prove innocence…. and they’re not going to voluntarily adopt a system that makes it difficult for them to do so.

Richard: Incredibly informed perspectives. Thank you for taking the time to publish… Not sure if you’ve heard, or have an opinion on the work over at id3 (idcubed . org), but they have an excellent piece on zero knowledge proofs, compliance and identity. Thought I’d point it out. Thanks again…

Link:https://idcubed.org/home_page_feature/privacy-and-compliance-by-design/

To much of banks in your blockchain future

Certificates are actually simply a transaction between a known cerified financial institution to a customers. If CHASE1 sends 5000 satoshi to 1Richard then CITI knows 1Richard is certified, so a certificate is simply a type of coloredcoin – KYCCoin. A wallet that supports KYCCoin simply has list of certified issuers. “Regulated” wallet would allow to transfer CITIUSD only to certified customers. Also, certifiers dont need to do kyc to customers that own their coins, because they will not transact with them, since customers could also redeem CHASEUSD in Citibank, but Citi and chase will have a clearing agreement between them.

Great article !

@yoniassia – really interesting idea… are you saying the simple act of sending BTC from CHASE1 to 1Richard tells the world that an “implicit” certificate exists? (i.e. CHASE1 wouldn’t have sent the satoshi otherwise!) And I guess CHASE1 could include extra data if they wanted to – some tags which specified which attributes they were vouching for? e.g. simply sending the coins would imply “IS_CUSTOMER” but they could also include “IS_AMERICAN” or “IS_PLATINUM” or whatever as extra data (for an extra fee?)

@chris – brilliant.. thanks… exactly the reason I blog these things…. I always end up learning more…. will go and read that now.

Exactly 🙂 ideally all you need is a group of financial institutions or even simpler a regulator to say – you are allowed to transact only with users that recieved kyc coin – potentially this can be even the goverment….

@yoniassia… how general can you make this? e.g. I envisage a system where “certifiers” vouch for different attributes I might possess. A bank might sign a certificate saying: “The holder of bitcoin address 1ABC is known to us”. A retailer may sign something that says: “The owner of this public key has spent $1000 with us over two years and never complained” – or whatever… i.e. a plurality of “certifiers”, each of which vouches for different facts about me….. with “me” being defined as a bitcoin address or public key or biometric.

Richard,

This is great thought provoking material and thanks for putting so much time into producing it. I am really excited about the possibilities for identity and the blockchain. I think a transformation in this area will lead to an exponential transformation in everything else.

The key take away here is that we have to separate the need to identify a person in the old model with the need to identify attributes in the new model. There are some mind blowing ideas here about what’s possible with “certificates”. Its reducing the need to identify the physicality of person every time they show up somewhere to having possession of something that’s cryptographically provable. The standard KYC and identity protocol focuses on tying out licenses, utility bills, IRS letters, bank statements and the like back to a physical address like its the best way ever invented to verify someone and or their business. The new model makes the almighty physical address attribute seem laughable in comparison. Kirk out.

@kirk – agree… and thanks 🙂

@ansel @richard re: “The burden of proof shouldn’t be on the accused to prove innocence”. Agreed but that is, unfortunately, a normative statement, Empirically, the reality is that many actors today live in a world where they *do* have to prove innocence…. and they’re not going to voluntarily adopt a system that makes it difficult for them to do so.

This is discussion is brilliant and gets to the core of what crypto is all about.

I agree that the proof shouldn’t be on the user. These are customers we’re talking about — people who are paying for a service from the bank (and, really, paying for all the services involved from each institution: banks and accounting and legal via fees (unnecessarily large ones!), government via taxes, etc.

But the way our financial system has evolved, the burden IS on the user and they ARE often treated as “the accused” (especially those who are poor or for other reasons live in shitty neighborhoods — bullet-proof glass, extra ID required, etc.). When we lived in small tribes, everyone knew your face and knew all these essential facts in question here. Financial and governmental institutions have taken on this role because we’ve grown bigger and more complex as societies.

But what all this is showing is a way forward (via back to basics!) where technology replaces what we once had in small tribes. We all agree to trust this new system and we all benefit (hopefully all trust it — there’s a giant education effort needed, that goes way beyond what’s already sorely needed in technology and digital currency, generally (see Marc Andreessen’s eloquent explanation here: Bitcoin Fireside Chat with Marc Andreessen and Balaji Srinivasan – Coinsumm.it: https://youtu.be/iir5J6Z3Z1Q?t=20m25s)).

It’s not only WAY much more efficient, it will be BETTER: I’d way rather trust a tech solution that is open to competition for better ways of organizing, securing AND EXPLAINING it, than what we have today: government monopoly on ID (on a platform that’s ancient, serviced by what is essentially a jobs program in disguise (I’m referring to the US here; probably better civil service in other parts of the world — and worse in developing countries)), and financial institution oligopoly on registration of assets.

sounds like a great idea. is there anything any of us can do to help out and move it forward even faster?