Twitter went mad last week because somebody had transferred almost $150m in a single Bitcoin transaction. This tweet was typical:

There was much comment about how expensive or difficult this would have been in the regular banking system – and this could well be true. But it also highlighted another point: in my expecience, almost nobody actually understands how payment systems work. That is: if you “wire” funds to a supplier or “make a payment” to a friend, how does the money get from your account to theirs?

In this article, I hope to change this situation by giving a very simple, but hopefully not oversimplified, survey of the landscape.

First, let’s establish some common ground

Perhaps the most important thing we need to realise about bank deposits is that they are liabilities. When you pay money into a bank, you don’t really have a deposit. There isn’t a pot of money sitting somewhere with your name on it. Instead, you have lent that money to the bank. They owe it to you. It becomes one of their liabilities. That’s why we say our accounts are in credit: we have extended credit to the bank. Similarly, if you are overdrawn and owe money to the bank, that becomes your liability and their asset. To understand what is going on when money moves around, it’s important to realise that every account balance can be seen in these two ways.

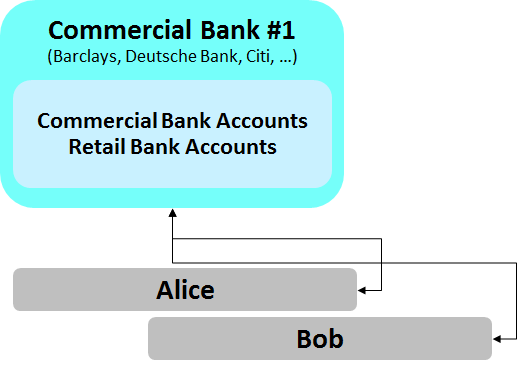

Paying somebody with an account at the same bank

Let’s start with the easy example. Imagine you’re Alice and you bank with, say, Barclays. You owe £10 to a friend, Bob, who also uses Barclays. Paying Bob is easy: you tell the bank what you want to do, they debit the funds from your account and credit £10 to your friend’s account. It’s all done electronically on Barclays’ core banking system and it’s all rather simple: no money enters or leaves the bank; it’s just an update to their accounting system. They owe you £10 less and owe Bob £10 more. It all balances out and it’s all done inside the bank: we can say that the transaction is “settled” on the books of your bank. We can represent this graphically below: the only parties involved are you, Bob and Barclays. (The same analysis, of course, works if you’re a Euro customer of Deutsche Bank or a Dollar customer of Citi, etc)

But what happens if you need to pay somebody at a different bank?

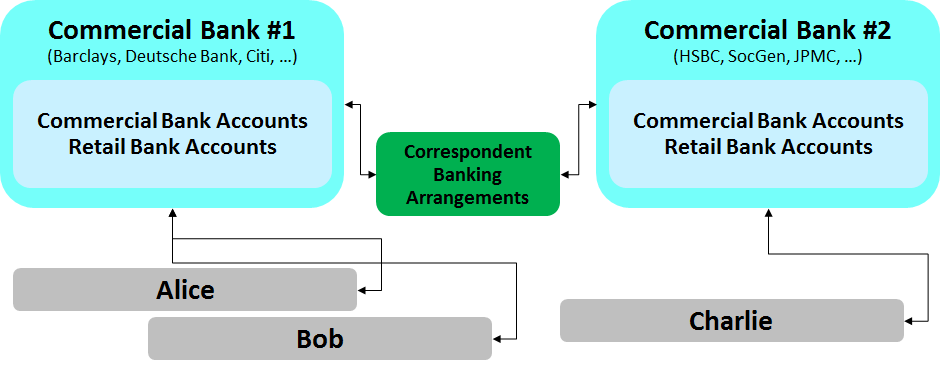

This is where it get more interesting. Imagine you need to pay Charlie, who banks with HSBC. Now we have a problem: it’s easy for Barclays to reduce your balance by £10 but how do they persuade HSBC to increase Charlie’s balance by £10? Why would HSBC be interested in agreeing to owe Charlie more money than they did before? They’re not a charity! The answer, of course, is that if we want HSBC to owe Charlie a little more, they need to owe somebody else a little less.

Who should this “somebody else” be? It can’t be Alice: Alice doesn’t have a relationship with HSBC, remember. By a process of elimination, the only other party around is Barclays. And here is the first “a ha” moment… what if HSBC held a bank account with Barclays and Barclays held a bank account with HSBC? They could hold balances with each other and adjust them to make everything work out…

Here’s what you could do:

- Barclays could reduce Alice’s balance by £10

- Barclays could then add £10 to the account HSBC holds with Barclays

- Barclays could then send a message to HSBC telling them that they had increased their balance by £10 and would like them, in turn, to increase Charlie’s balance by £10

- HSBC would receive the message and, safe in the knowledge they had an extra £10 on deposit with Barclays, could increase Charlie’s balance.

It all balances out for Alice and Charlie… Alice has £10 less and Charlie has £10 more.

And it all balances out for Barclays and HSBC. Previously, Barclays owed £10 to Alice, now it owes £10 to HSBC. Previously, HSBC was flat, now it owes £10 to Charlie and is owed £10 by Barclays.

This model of payment processing (and its more complicated forms) is known as correspondent banking. Graphically, it might look like the diagram below. This builds on the previous diagram and adds the second commercial bank and highlights that the existence of a correspondent banking arrangement allows them to facilitate payments between their respective customers.

This works pretty well, but it has some problems:

- Most obviously, it only works if the two banks have a direct relationship with each other. If they don’t, you either can’t make the payment or need to route it through a third (or fourth!) bank until you can complete a path from A to B. This clearly drives up cost and complexity. (Some commentators restrict the use of the term “correspondent banking” to this scenario or scenarios that involve difference currencies but I think it helpful to use the term even for the simpler case)

- More worryingly, it is also risky. Look at the situation from HSBC’s perspective. As a result of this payment, their exposure to Barclays has just increased. In our example, it is only by £10. But imagine it was £150m and the correspondent wasn’t Barclays but was a smaller, perhaps riskier outfit: HSBC would have a big problem on its hands if that bank went bust. One way round this is to alter the model slightly: rather than Barclays crediting HSBC’s account, Barclays could ask HSBC to debit the account it maintains for Barclays. That way, large inter-bank balances might not build up. However, there are other issues with that approach and, either way, the interconnectedness inherent in this model is a very real problem.

We’ll work through some of these issues in the following sections.

[Note: this isn’t *actually* what happens today because the systems below are used instead but I think it’s helpful to set up the story this way so we can build up an intuition for what’s going on]

Hang on… why are you making this so complicated? Can’t you just say “SWIFT” and be done with it?

It is common when discussing payment systems to have somebody wave their hands, shout “SWIFT” and believe they’ve settled the debate. To me, this just highlights that they probably don’t know what they’re talking about 🙂

The SWIFT network exists to allow banks securely to exchange electronic messages with each other. One of the message types supported by the SWIFT network is MT103. The MT103 message enables one bank to instruct another bank to credit the account of one of their customers, debiting the account held by the sending institution with the receiving bank to balance everything out. You could imagine an MT103 being used to implement the scenario I discussed in the previous section.

So, the effect of a SWIFT MT103 is to “send” money between the two banks but it’s critically important to realise what is going on under the covers: the SWIFT message is merely the instruction: the movement of funds is done by debiting and crediting several accounts at each institution and relies on banks maintaining accounts with each other (either directly or through intermediary banks). Simply waving one’s hands and shouting “SWIFT” serves to mask this complexity and so impedes understanding.

OK… I get it. But what about ACH and EURO1 and Faster Payments and BACS and CHAPS and FedWire and Target2 and and and????

Slow down….. Let’s recap first.

We’ve shown that transferring money between two account holders at the same bank is trivial.

We’ve also shown how you can send money between account holders of different banks through a really clever trick: arrange for the banks to hold accounts with each other.

We’ve also discussed how electronic messaging networks like SWIFT can be used to manage the flow of information between banks to make sure these transfers occur quickly, reliably and at modest cost.

But we still have further to go… because there are some big problems: counterparty risk, liquidity and cost.

The two we’ll tackle first are liquidity and cost

We need to address the liquidity and cost problem

First, we need to acknowledge that SWIFT is not cheap. If Barclays had to send a SWIFT message to HSBC every time you wanted to pay £10 to Charlie, you would soon notice some hefty charges on your statement. But, worse, there’s a much bigger problem: liquidity.

Think about how much money Barclays would need to have tied up at all its correspondent banks every day if the system I outlined above were used in practice. They would need to maintain sizeable balances at all the other banks just in case one of their customers wanted to send money to a recipient at HSBC or Lloyds or Co-op or wherever. This is cash that could be invested or lent or otherwise put to work.

But there’s a really nice insight we can make: on balance, it’s probably just as likely that a Barclays customer will be sending money to an HSBC customer as it is that an HSBC customer will be sending money to a Barclays customer on any given day.

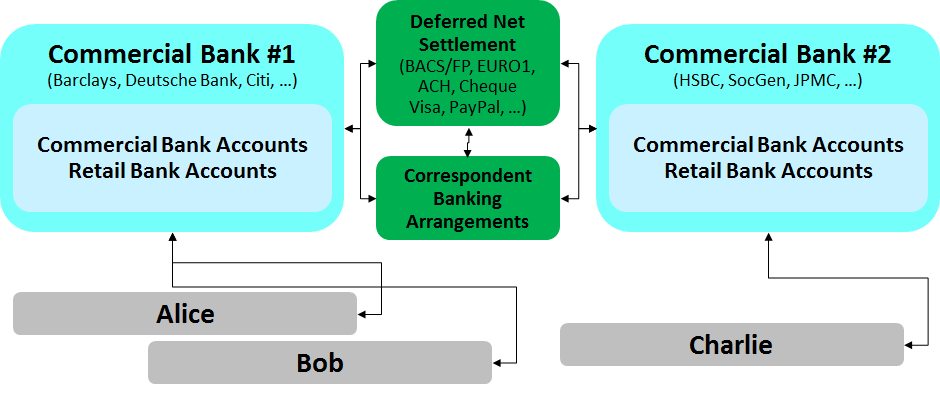

So what if we kept track of all the various payments during the day and only settled the balance?

If you adopted this approach, each bank could get away with holding a whole lot less cash on deposit at all its correspondents and they could put their money to work more effectively, driving down their costs and (hopefully) passing on some of it to you. This thought process motivated the creation of deferred net settlement systems. In the UK, BACS is such a system and equivalents exist all over the world. In these systems, messages are not exchanged over SWIFT. Instead, messages (or files) are sent to a central “clearing” system (such as BACS), which keeps track of all the payments, and then, on some schedule, calculates the net amount owed by each bank to each other. They then settle amongst themselves (perhaps by transferring money to/from the accounts they hold with each other) or by using the RTGS system described below.

This dramatically cuts down on cost and liquidity demands and adds an extra box to our picture:

It’s worth noting that we can also describe the credit card schemes and even PayPal as Deferred Net Settlement systems: they are all characterised by a process of internal aggregation of transactions, with only the net amounts being settled between the major banks.

But this approach also introduces a potentially worse problem: you have lost settlement finality. You might issue your payment instruction in the morning but the receiving bank doesn’t receive the (net) funds until later. The receiving bank therefore has to wait until they receive the (net) settlement, just in case the sending bank goes bust in the interim: it would be imprudent to release funds to the receiving customer before then. This introduces a delay.

The alternative would be to take the risk but reverse the transaction in the event of a problem – but then the settlement couldn’t in any way be considered “final” and so the recipient couldn’t rely on the funds until later in any case.

Can we achieve both Settlement Finality and Zero Counterparty Risk?

This is where the final piece of the jigsaw fits in. None of the approaches we’ve outlined so far are really acceptable for situations when you need to be absolutely sure the payment will be made quickly and can’t be reversed, even if the sending bank subsequently goes bust. You really, really need this assurance, for example, if you’re going to build a securities settlement system: nobody is going to release $150m of bonds or shares if there’s a chance the $150m won’t settle or could be reversed!

What is needed is a system like the first one we outlined (Alice pays Bob at the same bank) – because it’s really quick – but which works when more than one bank is involved. The multilateral bank-bank system outlined above sort-of works but gets really tricky when the amounts involved get big and when there’s the possibility that one or other of them could go bust.

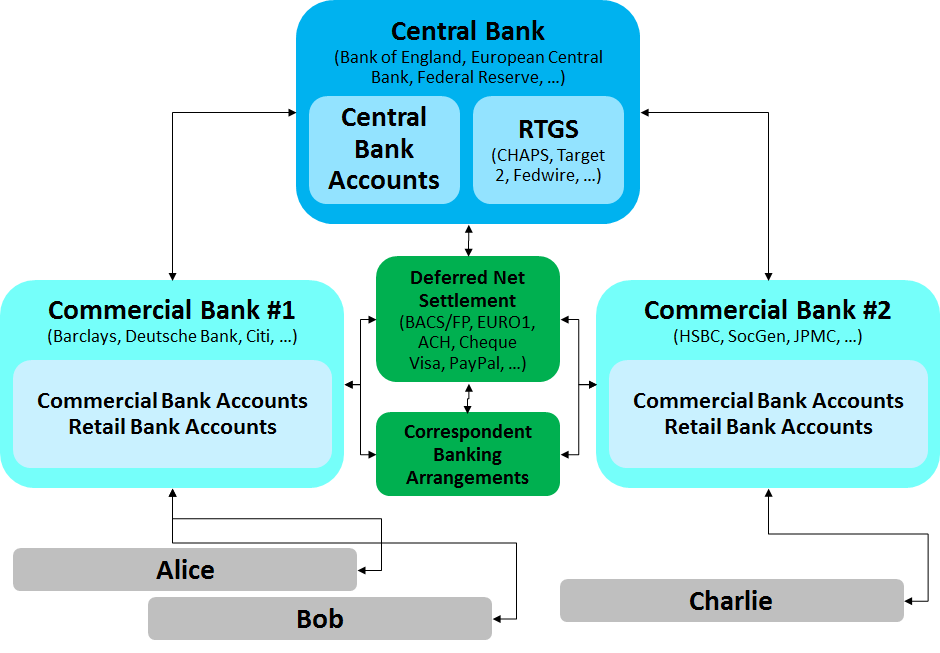

If only the banks could all hold accounts with a bank that cannot itself go bust… some sort of bank that sat in the middle of the system. We could give it a name. We could call it a central bank!

And this thought process motivates the idea of a Real-Time Gross Settlement system.

If the major banks in a country all hold accounts with the central bank then they can move money between themselves simply by instructing the central bank to debit one account and credit the other. And that’s what CHAPS, FedWire and Target 2 exist to do, for the Pound, Dollar and Euro, respectively. They are systems that allow real-time movements of funds between accounts held by banks at their respective central bank.

- Real Time – happens instantly.

- Gross – no netting (otherwise it couldn’t be instant)

- Settlement – with finality; no reversals

This completes our picture:

I thought this article had something to do with Bitcoin?

Well done for getting this far. Now we have a question: can we place Bitcoin on this model?

My take is that the Bitcoin network most closely resembles a Real-Time Gross Settlement system. There is no netting, there are (clearly) no correspondent banking relationships and we have settlement, gross, with finality.

But the interesting thing about today’s “traditional” financial landscape is that most retail transactions are not performed over the RTGS. For example, person-to-person electronic payments in the UK go over the Faster Payments system, which settles net several times per day, not instantly. Why is this? I would argue it is primarily because FPS is (almost) free, whereas CHAPS payments cost about £25. Most consumers probably would use an RTGS if it were just as convenient and just as cheap.

So the unanswered question in my mind is: will the Bitcoin payment network end up resembling a traditional RTGS, only handling high-value transfers? Or will advances in the core network (block size limits, micropayment channels, etc) occur quickly enough to keep up with increasing transaction volumes in order to allow it to remain an affordable system both for large- and low-value payments?

My take is that the jury is still out: I am convinced that Bitcoin will change the world but I’m altogether less convinced that we’ll end up in a world where every Bitcoin transaction is “cleared” over the Blockchain.

[Updated several times on 25 November 2013 to correct minor errors and to add the link to my Finextra video at the end]

I think for day to day transactions (buying groceries and so forth), players like Coinbase will start alleviating a lot of the pressure on the blockchain. In a similar fashion, they will act as a bank, only changing the numbers in between accounts.

Hi Simon,

I’m inclined to agree. I think there are two major forces driving us towards this sort of outcome. 1) the “average” user is likely to trust a reassuring brand more than themselves to manage their wallet, driving a move to a bank-like “safekeeping” business model and 2) the blockchain may not be the best vehicle for micro-payments. Combine those two observations and you end up with your prediction: there is a gap in the market for off-blockchain ‘aggregators’ of smaller transactions.

But I also know that many of the core developers, with infinitely more knowledge of the system disagree with this analysis!

Richard

Great post. Bitcoin protocol works well between untsted parties that know what are they up to, non reverse, etc. In this case, no need for a Central Bank. Most average users, as you say, still need trusted relations, so there will always be a trusted layer above Bitcoin for anyone in need for it, giving some space to the current retail banking model. Banks do have a place in the Bitcoin scenario, same as today, but the difference is that you could still operate without them if you wish. Banks will be just another option.

Excellent article Richard. I found myself asking a few questions as I read it, most of which you answered.

“CHAPS payments cost about £25”. Do they really, or is that just the price? Do they charge that much because they want to make money, or because they want to dissuade us from using that method or because they really do cost?

Are SWIFT messages signed? In other words if they contain non repudiation then surely they are a transfer of value rather than just the veil that you describe, however your focus is on whether the sender will go bust rather than deny sending it so it’s not relevant here.

Surely this whole thing is just an model to allow us to understand things. There’s still no actual value moving around, so it’s not much more true than just saying that you’re moving money. But of course it is a much more thorough model that allows you to do more things.

Surely bitcoin is still just the movement of liabilities. It still doesn’t have a real value until the sender gives up their sheep and the recipient receives a goat (or whatever else it is that makes the money have value to them). – I know you answered this by comparing to a gross settlement system rather than to real value.

Can I assume that currency exchange works the same way between central banks?

Nice explanation.

Also, for an understanding of modern fractional reserve banking, it’s worth watching the videos at http://www.positivemoney.org

Great article, it’s always easier to understand with small examples.

BUT I really didn’t like the graphs you did, mostly because the arrows go both ways. In the first example for instance, the arrow going from Alice to the bank shouldn’t go both ways. But it’s just my opinion.

@Jaumenuez I agree; I think we’ll see a federated model of the sort you describe – but, also as you say, with the option of going “direct” for those who know how to and want to

@benjamin – thanks. Good point re the diagrams; you’re right. The arrows are confusing. Sorry!

@sean – thanks for the link

@kassner – I left FX as an “exercise for the reader” but you’re right… the principles can be extended. e.g. imagine Barclays held a *dollar* account with Citi. That would give Barclays customers a way of making Dollar payments – and so on. Indeed, this cross-border example is what most people think of when you say “correspondent banking”. If you follow this line of reasoning, the counterparty risk problems becomes even greater and you end up with a need for an “RTGS for FX”, if you like. This motivated the creation of the CLS Bank.

@Sam:

* CHAPS – fair point. They’re “charged” at about £25. They probably cost a lot less.

* SWIFT messages – not sure if they’re cryptographically signed but the key thing that SWIFT offers that the internet does not is security at the end points and within the network. i.e. if you receive a SWIFT message purporting to be from Barclays, you can be pretty sure it *is* from Barclays!

* Bitcoin is interesting – because it doesn’t really fit the “liability” model. My holding of Bitcoins are nobody else’s liability. This makes them quite unlike any major currency today – and far more like gold or a commodity.

Reblogged this on CommonAccord and commented:

An explanation of how money clears the banking system. Didactic in the good sense.

Thank you very much for an interesting and educational blog post. I found it interesting because it sheds *some* light on a recent banking problem that left me quite stumped.

I recently attempted a $5000 bill payment from a debit account to a credit card, and due to a policy restriction, the bank holding the debit account canceled the payment. When I called their customer service department, they informed me of the restriction and told me I could try again that day. I tried again, and the payment went through fine. However, I was quite surprised when I checked my credit card account a few days later and discovered that both payments had been processed on their side leaving me with a $5000 credit balance! The debit account was only debited once. I called the credit card company and everything they could see on their end showed two successful and proper payments. I called the debit account company and spent over an hour on the phone with various people there, but none of them could find any trace of the duplicate payment. All they could see was the canceled bill pay and the successful one, but they couldn’t find any evidence of the extra $5000 that I received.

Of course, I’d love to just take the money and run, but I feel it is likely that one day, they will audit or balance their accounts and discover it, then come asking me for the money.

If you are interested, I’d love to get some insight into how this happened and maybe some tips on who I could ask to speak with that might be able to do something about it since it appears to be out of the league of the customer service department. I’m sorry for being a bit vague with the details, but I believe that this problem might actually be a reproducible flaw in their system, and I don’t want to set them up for fraudsters to take advantage of it.

@Daniel Einspanjer

Rinse, repeat. 🙂

Serioulsy, would be interested to find out what the result of this “error” ends up being.

Good explanation of the different transfer systems. Could you please add snippets of the following equivalents for India into the explanations at appropriate places?

1. Net settlement system done in batches several times a day – NEFT (National Electronic Fund Transfer) Monday through Saturday.

2. RTGS (it’s the same definition as above), done through the central bank – Reserve Bank of India. There is a minimum transfer amount of Rs. 200, 000 (called Rs. 2 Lakhs locally) for using RTGS, while there is no minimum for NEFT.

3. IMPS – Immediate Payment Service – instant, multiple channels (like SMS, web, etc.) and available 24 x 7 (unlike NEFT and RTGS that are not available on holidays and Sundays).

The fee for using these services varies across banks, amounts and account types.

@jorge — Yeah, I’m not about to try and see if it is a vulnerable flaw in their system. It is easily provable that the first time was an accident and I went to great lengths to document my notification to them. If I go trying it again “just to see if it works” I’d quite likely be facing criminal charges from them regardless of whether it is their own stupid fault for not listening to me.

I will be happy to follow up somewhere with details as to the result if/when it happens. For now, the money is just sitting in my IRA waiting for them to claim it.

Excellent tutorial, there. 🙂

From the viewpoint of teaching the basics to people with no professional finance background, though, there’re a couple of more questions I’d like to hear an answer for:

1. What’s the difference between commercial bank account and retail bank account? I’ve never heard of such terms.

2. If these international RTGS services do exist, what is it that’s retarding their use? If I make an account transfer from my bank to some account abroad, they’re always saying it’s going to take a long time. Are even the services of central banks so expensive that the real time transfer is only a service to those who are ready to pay more?

@jorge – ‘Launder, repeat’ perhaps would be more apropos? 🙂

This is a great quick read. For those who are interested in the Economics of Payment systems in detail –

Coursera has a course which goes in to the depths of the Economics of Money & Banking – https://class.coursera.org/money-001/lecture/index – by Prof. Perry Mehrling. Alternatively, you can find some of his Videos on YouTube.

Reblogged this on sheriken1234.

@indiasurfer – thanks for the comments. It’s great to get insight into the equivalent systems elsewhere.

Could you say a little more about how IMPS works? Who runs it? The central bank? A third party? Do funds ultimately arrive at a bank account? It sounds a little like a more advanced version of the UK’s Faster Payments service – in which funds are shown in recipients accounts immediately but the banks only settle amongst themselves every so often – but it would be great to hear more.

Cheers,

Richard

Reblogged this on Egill and commented:

Money talks, and sometimes even walks 🙂

Great article. Would it be possible for you to take some time to write a similar piece on securities trading and settlement. That would be awesome!

I have a question: If we already have a central bank system for moving money around, why do we still have the deferred net settlement systems like ACH around?

I like the idea of Myk, a piece on how security trading works, would definitely be worth reading, especially with T+2 or T+3 settlements.

visite http://www.placasparceria.com.br

Desenvolvemos Brindes Corporativos e Pessoais, Placas de Homenagem para diversas ocasiões, Placas Comemorativas, Medalhas, Trofeus, Gravação a Laser, Corte a Laser, Corte acrilico, Gravação Laser acrilico, Troféus em aço, Troféus Esportivos, Pins, Projetos Especiais, Campanhas Publicitárias, Crachás, placas anti-corrosão, placas de Inauguração, Chaveiros, Brindes Empresarias, no mais alto padrão de acabamento, Empresa localizada em São Paulo.

Thanks for the pretty thorough explanation 🙂

What I’m wondering: If the system is instant, why does a SEPA transfer still take a whole day to arrive?

Reblogged this on cum sa faci bani simplu si rapid and commented:

O explicatie simpla a modului in care Banii se misca in jurul sistemului bancar

Reblogged this on Leifdavidsen’s Blog and commented:

A fascinating, and mostly straightforward insight behind the curtain of the banking system by @gendal

This is worth reading a number of times. Always good to have a better understanding of something we use everyday, but don’t ever get told how it all actually works. As crucial to our lives as plumbing or electricity. Have reblogged it on http://leifdavidsen.wordpress.com/

Fantastic explanation. Never really understood this properly before, always kind of went over my head before reading this.

Nice read. Though I understand that there is a lot more to this than I care to know.

I have been reading the book “Lords of Finance” – the story of the great depression.

Reblogged this on Aut insanit homo, aut versus facit and commented:

A very clear look at the current banking system, and how bitcoin fits into the model.

Stellar writing Richard. What are your favorite books on this topic and banking/transactional processing in general?

@marinatin thanks for the feedback. I really like Alec Nacamuli’s book on payment systems (disclosure: he’s a colleague) and the European Central Bank did a great book on how securities processing systems work. From a business perspective, Celent often produce good papers on the custody business.

Reblogged this on TeckBiz.

Reblogged this on nehaanchalkar.

I got your blog @Mst. neha_anchalkar.

MT 103 799 AND 110, GET BACK TO ME IF YOU NEED IT FROM ALL TOP BANK IN UK AND USA

contact me here..james.mark963@yahoo.com..+1480-999-3964

Mr. Richard,

Have you ever heard about Ripple?

ripple.com

Hi my name is David, I want to show you how you can generate thousands dollars is automatically.Automatic Website Builder is the best website builder software on the market for creating, publishing, managing and monetizing new and existing websites with the help of Google AdSense and other pay-per-click and Clickbank, Amazon affiliate programs. Equipped with innovative features that are not available anywhere else, our automatic website generator enables you to build top-quality websites for virtually unlimited revenue. VISIT THIS LINK http://bit.ly/1jv2rUH

David- Great article. Wish you had a bitcoin tip address posted so I could show a little support! Another idea is that hopefully services like ChangeTip will integrate with WordPress soon.

Hi Richard – Really nice explanation of what is/can become a complex topic.

You may also consider adding something on how some deferred net settlement schemes/solutions have solved for the Settlement Finality problem – eg the use of authorisation systems and payment guarantees in use with the card schemes and similar with FPS.

@Mark – good point… do you have any links? I’d also like to know more about that topic 🙂

I understand so far – RTGS system as explained by your really applies to all the banks in one country having an account with the central bank. I however need to send money from country a to country b – it begs the question do central banks have their own central bank to central bank clearing system.

@Mendi – good question and yes. It’s called CLS Bank. Probably worth a post in its own right – but plenty of info on wikipedia, etc., about it and why it was created( namely: the failure of Herstatt Bank in 1974, which made it clear to everybody quite how much risk is hidden inside the correspondent banking system)

I shall research this bank – as I have never understood why correpondent banking had to be the only way. Thanks again

Why can’t International transfers simply go through the VISA network. Since international remittance is so expensive. And VISA is only 2-3%?

@sida – I guess we have to distinguish between international remittance and regular international payments. My guess is that recipients of remittances (typically) don’t have access to payment cards (hence remittance firms’ agent networks) and that regular international payments probably cost a bit less than an international visa transaction. Just a hunch though – it’s a good question

That helped a lot, great article! There are just a few things that I don’t understand though:

1) What happens when a customer of Bank A wants to send funds to a customer of Bank B when the two banks have different currencies and Bank A does not have enough funds at Bank B to complete the transfer? Lets also assume that Bank A also does not have enough funds at a path of correspondent banks or central banks to get to Bank B and that more money needs to be sent from A to B than from B to A.

I guess the gist is that Bank A’s accounts are underfunded at correspondent banks.

What must Bank A then do to complete the transfer? Must it send cash on a ship?

2) Also, how is it that my local bank has physical foreign currency notes for withdrawal?

Thanks

Hi! Do banks use their own bank branches as correspondent banks? For example, can BNP Paribas in France us BNP Paribas in New York as its correspondent bank account?

@Charly – 1) I guess you’re talking about the problem of liquidity management, etc. One option is for the short bank to buy what it needs on the FX market (e.g. if they’re a British bank, find a counterparty somewhere who is willing to sell the target currency for pounds). Another option is to delay the payment… i.e. defer paying out until enough funds to cover it have arrived, etc

2) Not sure why this would be a problem… think of the bank as a retailer… they have some foreign currency in stock (in their inventory), which they have presumably already paid for. And they recoup the cost when they sell it to you.

@MZ – Good point. Banks certainly do use their overseas entities to make payments abroad. So perhaps one way to interpret my piece is to think of smaller regional banks that don’t have their own international network.

Very informative!

So sidechains become interesting when you consider bitcoins future is arguably as the RTGS for cross border transactions without countries that don’t have reliable central banks or correspondent banks.

I’m curious if stellar could be a bitcoin sidechain. So you get a layered model.

P2P payments

Custodians to manage that as a liability on case of lost or stolen devices

Stellar and other sidechains facilitate inter p2p service transactions and custodial relationships

The Custodians then use bitcoin as an RTGS where there is no central bank.

An excellent article

Somebody pointed out to me in private conversation the other day that you don’t need a sidechain to integrate with stellar/ripple – a gateway is all you need!

It should be technically trivial to scale up the transaction volume to “PayPal-level” (I’m actually working on code to test that right now); scaling up to “Visa-level” will be trickier, but processing financial transactions is much easier than all the other things computers can do quickly (video, speech recognition, 3D rendering…) nowdays.

I’ll be pushing to keep Bitcoin transactions cheap and accessible to everybody, not just people with millions of dollars to move around.

@gavin – thanks for the comment. It’s a fair point… we do have to look at large numbers in context and with the perspective of time. e.g. imagine all 2bn internet users wanted to do one on-blockchain transaction per year. You’d need to be able to process about 64tps (I think. I really hope I didn’t screw up the maths). So, allowing for EVERYBODY to do one a month would need about 1000tps (ignoring for now that peaks would be way in excess). Assume 250bytes/tx and you’re looking at about 21Gb per day…. about 100Tb per year. A petabyte for a decade of transactions. 10^15 or so, give or take an order of magnitude.

Now some people will need to do far more transactions but not everybody is going to use a system like this so perhaps these are reasonable numbers to play with.

10^15 *sounds* like a lot — and maybe the real requirement is higher…. but we already know we’ll have to deal with at least 10^21 bytes routinely in the broader IT industry a few years from now. And the idea of storing this on thousands of nodes is obviously troublesome. But it’s not *obviously* insane (well, maybe a little bit insane).

Hello Webmaster do you want unlimited content for your site?

100% unique and human readable. Type in google:

Nyschash’s Rewriter

Hi Richard,

Thank you so much for such an informative and clear explanation on the topic. I would like to ask a question, hope you could kindly enlighten me. If the Central bank system can eliminate all the key risks involved in the “transfer” money among the banks, why would banks still using defer net settlement systems? What are some of the types of transactions that works better with defer settlement and why?

Thank you so much for your time and attention!

Sheng,

Singapore

Hi Richard,

Great article. As a corporate treasurer what would consider the biggest risks I need to be aware of in making international payments and other then ensuring accuracy of the payments details and mitigating against internal fraud what can you do about them.

Thanks

Peter…

‘there is a gap in the market for off-blockchain ‘aggregators’ of smaller transactions’ – the real problem with bitcoin is the incredible waste of energy. just SUCH a waste. awful. ie joules.

Reblogged this on O2O BL0G - まめメモ and commented:

it:s amazing!!

Nice article!! Now lots of people can be understand that which way money moves around the banking system, thanks for sharing with us.

I enjoy, lead to I discovered exactly what I was having a look for.

You have ended my four day lengthy hunt! God Bless you

man. Have a nice day. Bye

Thanks for the crystal clear explanation. My next query – for international exchanges – where there is a net amount of money owing from one country’s citizens to another country’s citizens, is there ever a real transfer of …. something? Would this something be what I’ve heard to be “reserves in such-and-such a currency” held by a central bank?

Fascinating subject…. Frank

frank – great question. I don’t know for sure but my thinking would be something like this. Let’s imagine lots of citizens of country A want to move their money out, perhaps to country B. What would that look like? The end-result would be that citizens in country A are owed less of currency A by the banks of country A and more of currency B by the banks of country B, right? So why would the banks of country B agree to owe them more?

For me, I guess there are really only three options:

1) The banks of country B are willing to increase their holdings of country A’s currency (either in the form of reserves at country A’s central bank or by being owed more of country A’s money by the banks of country A). They’d presumably only be willing to do this at an unfavourable exchange rate in times of stress? The result would be the sending currency’s value dropped, exascerbating the problem I imagine?

2) The banks (or central bank?) of country A hand over some of their holdings of country *B* currency, to the extent they have enough and are willing to. I think this is your “reserves transfer” scenario, right? Again, this can only work for so long: eventually the bank(s) will run out of foreign reserves. Perhaps this is similar to what happened to the UK on Black Wednesday? (http://en.wikipedia.org/wiki/Black_Wednesday). i.e. you can think of the central bank in this scenario as using their foreign holdings to purchase its own currency from those wanting to sell it, perhaps with the intent of propping up the price. In this scenario, those selling Currency A then store the country B currency they’ve acquired from the country A central bank at a bank in country B

3) The banks of country B buy/accept *assets* in country A. Imagine you own a factory in country A. Rather than selling it then transferring the money out, you simply sell it *for* foreign currency. Alternatively, you could imagine this being intermediated by the banks. i.e. when you ask your bank to buy Currency B for you, they “pay” for it by handing over assets they own in country A.

This really isn’t my area of expertise, however, and working things out from first principles can often lead people astray… so please only treat this as a suggestion for how it works..!

Hi Richard,I really want to thank you for the clear explanation about the swift, and the example given 🙂

Thanks for your suggestions Richard – in response to my question on the same day – May 17 2015.

Without me having more formal knowledge of international banking and finance, all three of your suggested mechanisms (transferring foreign reserves) would probably work in different circumstances. I checked out the Black Wednesday reference, and in principle, running out of foreign reserves may have been the reason that defending the UK Pound may have failed – though it spoke of the “speed” at which trades were completed, at which point I realised I needed to know more to understand this.

I am continuously amazed at how seemingly ‘simple’ concepts, such as representing value of goods / services by a currency, or IOU, can become so incredibly involved: And useful to those who understand it.

Thanks you again for your explanations and insights.

Hi Richard, I’m struggling to understand the swift message MT202, please assist.

HelloRichard Gendal Brown,please can you tell me about Draft ,because one company want to do project true my company but he want to send 50Million Draft to my bank,also i don’t know anything about draft payment can you please help me out maybe is good to or not so i can know next step to take thanks

HelloRichard Gendal Brown,please can you tell me about Draft ,because one company want to do project true my company but he want to send 50Million Draft to my bank,also i don’t know anything about draft payment can you please help me out maybe is good to or not so i can know next step to take thanks

hi can anyone on here please help. my husband who works abroad is paid using SWIFT and some payments are lost and do not

reach the receiving bank inspite of instructions on SWIFT always being the same. an intermediary bank is used as payment is

in USD and is being converted to uk pounds. The remitting bank is Barclys and intermediary is also Barclays. can someone please help.

If you’re looking to find a swift code for the bank you’re trying to send money to, you can use: http://bank-code.net/

It list all banks in the world and their associated swift code, along with a breakdown of the actual swift code so that you can understand what it means.

Here’s an example for BARCLAYS BANK PLC bank located in NEW YORK: http://bank-code.net/swift-code/BARCUS33XXX.html

I hope this helps you guys.

Thank you for the fruitful information. I am from Myanmar and I got a presidential scholarship from my government. I got CAS from one of the universities in UK and today, I just transferred all the school fees to the university bank account which exists in Barclays Bank PLC in UK. Banking system in my country is still in the progress, so they don’t have a direct connection with banks from UK. The officials from the bank said that my money would go to Singapore first and then to UK. They said the money can be surely transferred to Singapore but they are not sure whether Barclays bank will accept my money. They also warned me that my money can be transferred back to my country or even BLOCKED for the worst. It concerns me a lot and I will sit for Visa interview within a few days. In which conditions my money will be transferred back to me or blocked? It is not black money and I don’t do any illegal tradings. I am just a simple student. Could somebody explain me? Thanks.

@WMET – Sorry to hear about the uncertainty (and congratulations on the scholarship and CAS). Short answer: I don’t know, sorry. Payments are often blocked if they are to/from people/accounts that are known to be suspicious. That doesn’t seem to be the case here, right? Have you spoken to the university? Perhaps they can speak to their bank to inform them the payment is coming and that it is expected? Sorry I can’t offer any more help than that. Best regards and good wishes for your studies.

Thank you so much. I will inform my school as you suggested. I hope it will help me a lot. Have a nice day. 🙂

I think this is a great article that I have been looking for, as people often too easy to spell SWIFT and think they know all. One question though — how do banks “deposit” money to a Central Bank? In the RTGS model, wouldn’t a bank need to keep a lot of deposit in Central Bank for settlement?

Hi Gendal, another question about MT103 — in this message it only says what are the ordering and receiving customer’s account numbers are. But it does not say what the bank’s reciprocal account numbers are. Are the reciprocal account numbers part of SWIFT setup agreement (something pre-agreed between banks) so they are not required in MT103? Thanks.

The outcomes are ambiguous however it seems that Dr.

Winstock believes darknet markets could do more great compared to damage.

Echt cooler Artikel über Browsergames.Ich werde nochmal auf dieser seite schauen

Nice and Very informative blog on money and banking system.

This is the right blog for everyone who wishes to find

out about this topic. You understand a whole lot its almost hard to

argue with you (not that I really will need

to…HaHa). You definitely put a new spin on a subject

which has been discussed for ages. Wonderful stuff, just wonderful!

Very good article, thanks.

I actually came across the article whilst trying to establish if the following:

1) Are there any existing practices for effecting payments where the Beneficiary has requested to be paid in a currency in which they (Beneficiary) & their Bank does NOT hold any (Vostro) account in?

2) More specifically also, if the Paying Bank sends an MT103 in the currency requested to the Bank which holds an account in that currency with them (Paying Bank) & which (MT103 Receiving Bank) also maintains a different (Vostro) account for the Beneficiary’s Bank[& the paying bank places cover funds in the currency requested in the (Vostro) account of the MT103 Receiving Bank]:

a) Is there any practice the MT103 Receiving Bank can use to pass on the MT103 (& related cover funds) to the ultimate Beneficiary’s Bank &

b) More specifically, can the MT103 Receiving Bank (unilaterally) convert the payment into the currency in which they maintain a (Vostro) account for the Beneficiary’s Bank, place the cover funds (in the new currency) into the (Vosto) account of the Beneficiary’s Bank with them (MT103 Receiving Bank) & send an enhanced MT103, either:

(i) In the original (instructed) currency (& amount), specifying that cover funds are placed (& providing exchange rates used, charges taken, etc, in Field 72, etc) or

(ii) In the new currency (& amount), specifying that cover funds are placed in the (uninstructed currency) Vostro?

Richard,

Though I am not from a financial background, your article has helped me in developing an opinion about the banking between banks. A simple example like this really makes it easy to grasp the concept.

Thank You

great article, I work in bank IT and never really thought about this before. Anyone have any similar articles on how money is created?

Can you please clarify something for me? I understand that, for risk considerations, banks are using central banks’ settlement accounts rather than other banks’ settlement accounts. That being said, why would one need to be using another bank’s settlement account at all? All banks could simply solely use the central bank for that purpose. thanks

Thanks so much for this explanation, Gendal. I’ve spent the entire day trying to learn what actually happens between banks when you “send” money to someone. Almost everything else I’ve found glosses over the technical details, which is incredibly frustrating. Your description here is easy to follow and understand. Cheers for making knowledge and understanding accessible to the masses.

This may seem like a inane question, but I am wondering if you can assist. The above explanation of how money is transferred is extremely helpful. In relation to RTGS I fully understand how this can result in settlement finality and importantly zero counter party risk. However, it got me thinking how do banks transfer money into their respective Central bank account electronically. Does the Central Bank have a correspondent relationship with each of the member banks? If it doesn’t, how would they debit/credit their respective accounts to facilitate the transfer. Alternatively, if the Central Bank does hold an account with the member banks, does this not put the Central Bank at counter party risk? As the commercial bank could simply credit the liability account of the Central Bank , and in turn debit their asset holding at the Central Bank when they want to hold cash at the Central Bank. Consequently, the Central Bank would credit the liability account of the commercial bank and debit their asset holding at the Commercial Bank (an obvious counter party risk).

Am I missing something? Any assistance would be greatly appreciated.

The question thats brought me to this article is still not answered. Or if it is, I didn’t understand.

How do banks actually settle their balances? Do they send trucks with cash, gold, etc… How does that work for foreign currencies?

Have you ever lost access to an email that contains 70% or more of your business or work or family details and don’t know how to recover this? do you think someone regularly tries to get into your postpaid mobile carrier or Netflix account etc? Then you should send a mail to Termitehacking at protonmail dot com to resolve all….you don’t need to thank me.

HOW CAN I INVEST ON BITCOIN

Hello everyone, Are you looking for a professional trader, forex and binary manager who will help you trade and manage your account with a good and massive amount of profit in return. you can contact MRS. LINDA KATINA for your investment plan inorder to get started. for She helped me earned 12,000usd with a little investment money. Linda Katina, you’re the best trader I can recommend for anyone who wants to invest and trade with a genuine trader, She also helps in recovery of loss funds..you can contact her on her Email: lindakatina@yahoo.com

HOW TO INVEST ON BITCOIN AND MAKE ALOT OF PROFIT

Unbelievable, I thank Almighty God for what

Mrs Linda Katina did for me. I’m really happy to receive my profits, ma’am is because of you I’m smiling now. You are the best manager I have ever meet.

I enjoyed my trade with your platform,

I’m really grateful, thank you very much ma’am for making my dream of having a beautiful house and a nice car. Thank you because of you my family is happy and this is my best moment Ever.

Hello everyone Mrs Linda Katina is real and legit, Invest in her company, she is the best.

You can contact her via email on lindakatina@yahoo.com

Oh my God, thank you for making me rich in binary options trading and I want to use this medium to thank you Mrs Linda Katina for helping me to make money through online Bitcoin trading. I only Invest with $1000 and I received my profit of $5000 in just five days of trading ma’am you are the best and thank God that I believe in you. You all can invest with her. She is the best account manager. And her company is real and not a scam. Once again thank you for making me happy. You can also reach out to her via email on lindakatina@yahoo.com

HOW CAN I INVEST ?

Hello everyone, Are you looking for a professional trader, forex and binary manager who will help you trade and manage your account with a good and massive amount of profit in return. you can contact MRS. LINDA KATINA for your investment plan inorder to get started. for She helped me earned 12,000usd with a little investment money. Linda Katina, you’re the best trader I can recommend for anyone who wants to invest and trade with a genuine trader, She also helps in recovery of loss funds..you can contact her on her Email: lindakatina@yahoo.com

HOW BITCOIN WORKS

I will forever be grateful to Mrs Linda Katina due to your strong and good skills and trading strategy, I was skeptical at first of the test but I called courage and tried it, here, I restored everything to a very big turn out with a great trade and Management she has guided me and given me super amazing results. Thank you so much, Mrs Linda Katina. I have received my profit in my bitcoin wallet. Thank you very much you are the best

Contact her on lindakatina@yahoo.com

HOW TO INVEST ON BITCOIN

Hello everyone, Are you looking for a professional trader, forex and binary manager who will help you trade and manage your account with a good and massive amount of profit in return. you can contact MRS. LINDA KATINA for your investment plan inorder to get started. for She helped me earned 12,000usd with a little investment money. Linda Katina, you’re the best trader I can recommend for anyone who wants to invest and trade with a genuine trader, She also helps in recovery of loss funds..you can contact her on her Email: lindakatina@yahoo.com

HOW PROFITABLE IS BITCOIN MINING

Oh my God, thank you for making me rich in binary options trading and I want to use this medium to thank you Mrs Linda Katina for helping me to make money through online Bitcoin trading. I only Invest with $1000 and I received my profit of $5000 in just five days of trading ma’am you are the best and thank God that I believe in you. You all can invest with her. She is the best account manager. And her company is real and not a scam. Once again thank you for making me happy. You can also reach out to her via email on lindakatina@yahoo.com

Unbelievable Mrs Ariana Elvira , I’m really happy to receive my profits, ma’am is because of you I’m smiling now. You are the best manager I have ever meet.

I enjoyed my trade with your platform,

I’m really grateful, thank you very much ma’am for making my dream of having a beautiful house and a nice car. Thank you because of you my family is happy and this is my best moment Ever.

Hello everyone Mrs Ariana Elvira is real and legit Invest in her company she is the best.

You can contact her on email bitcoininvestmentb48@gmail.com

I advise everyone to be careful with who you trade with. I have been trading with Mrs Linda Katina and everything has been working perfectly. So many people are saying profits cannot be made from trading online, I use to believe that.

But now it is clear to me now that trading online is real. Is just that so many people are not opportuned to meet managers like Mrs Linda Katina who is going to work you through success in binary option trade. Write Mrs Linda Katina on WhatsApp +19738332804

I Am short of words for the amazing way SWIFT ACCESS helped me recover my Bitcoin in just 2 weeks, I doubted at the beginning, because of my past experience so I didn’t know how to trust them because of the amount of Bitcoin I have lost in the hand of scammer, , if you have ever lost your Bitcoin or any crypto issue I recommend you contact: swiftaccess37 (*_[]at_*) gmail com

you can thank me later.

It is possible to recover your money back from scammers. with the improvement in technology. Every invention has a solution ways to track the source. It can only be done by an experts and legitimate recovery firm. Contact[

instantrecovery12 (*At*).com

] is you need help on recovery your stolen fund and bitcoin.

An interesting discussion is worth comment. I think that you should write more about this topic, it may not be a taboo subject but usually folks don’t speak about such issues. To the next! Cheers!!⚡ 😏 2021-09-24 00h 37min

I am a victim of bitcoin scam. After I got scammed, I didn’t hear from the scammers again. They ignored all my messages. I contacted FBI but they couldn’t do much. I ran into debts and found it difficult to live. A friend introduced me to a fraud specialist who I contacted. I thought all hope was lost until this specialist helped me in recovering my money. You can reach him through his gmail address with Instantrecovery12 (*at*****) GMAIL COM. If you are a victim of any kind of scam, don’t give up, all hope is not lost. Can’t believe I’m still alive to write this because at some point in my life I thought I wasn’t living.

It is year 2022 and this article is as much as relevant today as it would have been in 2013. Including the bitcoin commentary. Thank you for making it simple for everyone to understand.

Hello,

We Offer Swift MT760 BG/SBLC, FC MTN, Letter of Credit { LC }, MT103Etc.

N/B: Provider’s Bank move first.

Let me know if you have any need for the above offers.

Thanks

Name:Jerry Osborne

Email:osbornej715@gmail.com

Skype:osbornejerry123@outlook.com

I’ll advice you to use the services of a reliable IT expert / Recovery expert to help you retrieve all your lost or stolen bitcoin on the bitcoin network from scam brokers and fake investment platforms (Websites, blogs and forums). His services are outstanding and you can contact him at INFO AT CYBEROPERATIONS, TECH. Perfectly quintessential service.

Great article, though for the Bitcoin scaling problem it would have been nice to mention the Lightning network, which is a second layer scaling solution that enables fast and cheap Bitcoin transactions similarly to the banking systems mentioned here, which only settles the balances in the Bitcoin network in the end. It’s very similar: if A owes B owes C owes A 10 units, that balances out and no settlement needs to be recorded in the main layer/structure.

I suggest using Pro Wizard Gilbert Recovery for all of your cryptocurrency and digital asset recovery needs. They assisted me in recovering my money because I was one of their clients. When it comes to recovering cryptocurrency, they truly are the finest. My money was placed on a bitcoin trading platform that went down earlier this month. Pro Wizard Gilbert Recovery was able to retrieve my money from the crashed platform when I got in touch with them after finding their website. I am posting this here for everyone to see since it made me so happy. You can get in touch with Pro Wizard Gilbert Recovery using the details listed below.

Email: prowizardgilbertrecovery(@)engineer.com

Thanks.

The only person capable of assisting you in recovering your money from scam brokers is a professional financial recovery service called Alister Recovery. I recently received help from them to retrieve my lost funds. Many of these binary option companies are scams, and their weak database security makes them vulnerable to exploitation. Alister Recovery possesses special recovery tools, root recovery tools, and technical infiltration strategies that can easily exploit these vulnerabilities. Their skilled team of professionals specializes in infiltrating company databases, extracting files and documents, decrypting transaction details, and recovering stolen funds. To get in touch with Alister Recovery, you can reach them at AlisterRecovery ART GMAIL [[DOT]]Com.

My misplaced cash of roughly $180k were found and recovered. I had my trading money unloaded by a broker who for three months refused to give me access to my trading account, and I had no idea that I would be able to recover it. That I could get my money back without any hassle makes me quite happy. Elite Wizard Bitcoin Recovery, who earned a reputation as a licensed binary options recovery specialist, is a technician I would really like to thank. Your broker manager is recommending that you make further deposits before making a withdrawal if you have money in your account that you intend to take out. Please get in touch with Elite Wizard Bitcoin Recovery using the information below if you are unsure how to proceed. In a matter of days, they will demonstrate to you the guild lines to recover your stolen funds.

Email: eliterecovery247@cyber-wizard.com

Phone: +1 (740) 688-0116

I met someone on an online dating app. At some point, the scammer instructed me to send crypto assets to what I believed was a legitimate banking app based in Singapore. But the scammer provided fake instructions so that my money went into the crypto asset wallet belonging to the scammer instead. I deposited Ethereum (ETH) into the scammer’s account on three separate occasions, eventually losing thousands of dollars. I hired HACKWEST AT WRITEME DOT COM who specializes in crypto assets recovery and other hacking services and was able to locate the scammer’s wallet through blockchain forensic analysis and was able to retrieve my entire funds they stole from me. It’s about 673,000 USD in total. Although Hack West didn’t do this for free, it was worth it. I will always tell everyone about my experience with West and his team.

Hi Guy’s

FULLZ AVAILABLE

USA UK CANADA All States & Cities available

Fullz with DL available as well

FRESH SSN DL FULLZ DLSCAN MVR MMN HIGH CS PROS SHOP TELE: leadsupplier

USA SSN DOB DL ADDRESS|DL SCAN (front+Back+ssn)

UK NIN Dob DL ADDRESS SORT CODE|DL SCAN (Front+Back+Selfie)

CANADA SIN DOB DL ADDRESS MMN PHONE EMAIL|DL SCAN (Front+Back+Selfie)

High Credit Scores Pros 700+ with DL Scan Docs

W-2 Form with employee fullz

Real DL SCAN with selfie & SSN plus Driving Docs

Young & Old Age Fullz of every state

CC with CVV & Dumps with pin 101 & 202

Passport Photos with Selfie

CA-AU-UK-RU-IT-FR-GR ETC DL Scan available

SMTP|RDP|C-Panels|Web-Mailers

Carding, Cash Out, Dumps Cash out Tutorials

SMTP Linux Root

CC Cash out & Transfers Methods

Genuine Stuff

Valid & Guaranteed

24/7 available

No testing for Tools, CC’s & DLscan

Docs for KYC available as well

What’ App : +1.. 7577.. 886.. 129

Tele : @ leadsupplier / @ killhacks

Skype : @ peeterhacks

E mail : dghacks2 at g mail . com