Shared ledgers could be revolutionary but do we need to share a mental model for banking to make sense of it all?

What would be your first instinct if your friend were to tell you they had £1m in the bank? To congratulate them on their good fortune? To suppress a pang of jealousy?

Wrong, wrong, a million times WRONG!

The only acceptable first instinct is to shout loudly at them: “No! You fool! You don’t ‘have’ a million in the bank. You have lent a million to the bank. They owe it to you. How could you reveal so casually that your mental model of banking is so wrong?!”

If your first instinct was the correct one then you need read no further; there is nothing for you here. But, for everybody else, you could be missing something really important. And this could matter: as I’ve written repeatedly, we could be witnessing the emergence of shared ledger systems in finance – blockchains, if you prefer. And they will be used to record obligations of – and agreements between – firms and people of all sorts. A more complex (and larger) example of this, if you like:

The four-column model of shared ledgers

To make this work, we’re going to have to get a lot more precise about how we think about financial relationships. And I’m pretty sure it all comes down to having a clear mental model for balance sheets.

What is a balance sheet?

Imagine you were starting a bank. You’d want to put a system in place to keep track of the finances: how much cash do you have in the vault? To whom do you owe money? How much have you lent out? And so on.

The basics are not rocket science and there are only two key reports at the heart of this: the balance sheet and the income statement (aka the P+L).

They exist to answer two important questions:

- What do I own and how much do I owe? This is what the balance sheet tells you. Think of it as a point-in-time snapshot.

- How did I do in the last period? That is what the income statement tells you. Think of it as the story for how you got from last year to this year.

In this piece, we’ll look at the balance sheet, because I think it’s the one you need to understand to make sense of where shared ledger technology could be going.

And the good news is: a balance sheet is simple… it’s just a two column table:

- You write all the things you own – your assets – in one column

- You write all the things you owe – your liabilities – in the other column.

- If you own more than you owe, the difference belongs to your shareholders: their “equity” is what makes it “balance”.

- If you owe more than you own, then you’re bankrupt (“insolvent”):

A balance sheet only has two important columns: what you own and what you owe.

Let’s open a bank!

So now let’s imagine you’re ready to start your small bank, “GendalBank”. Your friends think it looks like a good bet so they’ve agreed to contribute towards the £1m you need to get it up and running in return for shares.

£1m to start a bank?! As you can tell, my example is going to be very unrealistic indeed…

It may be obvious but I’ll say it anyway: they have no right to ask for this money back… it’s not a loan. But if you closed the company down, anything that was left after you’d paid off all your employees, suppliers and lenders, etc., would be returned to the shareholders.

So what they really have is a residual claim on the company. That’s what equity is. And when you look at it this way, it’s obvious that equity is a liability of the company: GendalBank has an obligation to return what’s left over to the shareholders if it ever closes down.

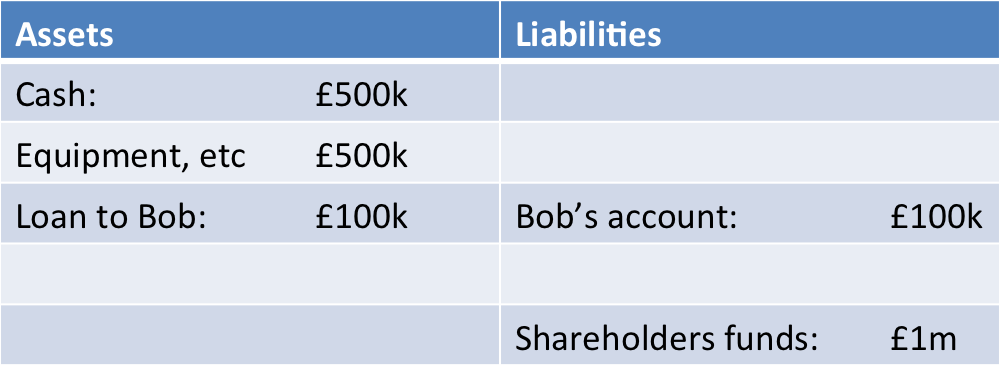

So GendalBank has been set-up and the shareholders have handed over their £1m. How would we draw up a balance sheet to reflect all this?

GendalBank’s balance sheet after the shareholders have paid for their shares. (Pedants: please forgive me… I omitted the trailing apostrophe on “Shareholders’ funds”. I don’t have time to update ten diagrams… but I can assure you the mistake pains me more than you)

It’s as exactly as we’d expect. Your new bank has £1m in cash – maybe you’re holding it in a vault or perhaps you’re holding it at the Bank of England. But, either way, this cash is now GendalBank’s… it doesn’t belong to the shareholders any more; it belongs to the company. It’s the bank’s asset now. It can use that cash for whatever it likes. So we note it down in the assets column.

And remember what the shareholders have paid for: a residual claim on the company. Well, there are no other claims on the company right now, so we record a liability to the shareholders of £1m. If we closed down right now, they’d be entitled to be paid £1m.

It bears repeating: bank capital is a liability. And this turns out to be a really useful thing to know. Because it allows you to spot charlatans at a thousand paces… any time you hear somebody talking about capital as if it were an asset of the bank (“holding more capital” is a great giveaway) then you know they don’t know what they’re talking about…

(I can’t help thinking making statements like that opens me up for all kinds of ridicule when the faults of this piece are identified…)

Great… so now we buy some IT equipment and an office with some of that cash. So perhaps the balance sheet looks like this at the end of the first week:

We use some of the cash to buy some equipment and an office, etc

To keep things really simple, I’m going to assume the bank has no expenses. I did say this was a very unrealistic example! So we’ll assume we own the office and that there are no employees to pay. This is just to avoid having to look at the income statement for now.

And now we’re open for business… time to make some loans…

Bob walks in off the street and asks to borrow £100k because he’s planning on buying a very nice car at the weekend. He looks a trustworthy sort so we make the loan.

And now another really interesting happens: we create money out of thin air…

Our loan to Bob has created money out of thin air!

Now Bob hasn’t withdrawn any money yet – he’s not buying the car until the weekend, remember. But look at how counterintuitive the balance sheet has become.

Look first at the asset side: we still have £500k cash, of course: he’s not drawn anything out yet. And we see the £100k loan to Bob. That’s our asset since Bob is obliged to pay us back £100k in the coming months and years. That’s a valuable promise to hold – it’s an asset of the bank, for sure.

Aside: just as above, I’m making some massive simplifications here, not least that I’m completely ignoring interest rates and discount rates, etc. Humour me 🙂

And now look at the liability side: it records that we owe £100k to Bob. That’s fair enough. If he looks at his account, he’ll see £100k there that he can withdraw whenever he likes. As far as he’s concerned he thinks “has £100k in the bank”.

So we have £500k of our own cash – either in the vault or at the Bank of England. And Bob thinks he has £100k “in the bank” as well.

Hang on… what’s going on? Did we just turn £500k into £600k by updating a spreadsheet?! Or does this mean that £100k of the £500k is now Bob’s? Or what?

The way to understand this of course is to observe that the £500k is our asset , whereas the £100k is Bob’s asset – and our liability. They’re not the same thing at all and it makes no sense to compare them in this way.

And so here’s another way to spot a charlatan: if you ever hear somebody talking about bank deposits as if they’re assets of the bank, you know you can safely ignore anything that person says… As this example makes clear, bank deposits are liabilities… and you have to be careful around them… because customers have the annoying habit of asking you to give them the money so they can spend it on something. And, to do that, you’d better have enough cash (on the asset side of your balance sheet, remember) to be able to honour that request.

This is what people mean in this context when they discuss “liquidity” – do you have enough cash or stuff you can quickly turn into cash to meet withdrawal requests from your customers?

Aside: in many ways, this conundrum is the absolute heart of banking: how to manage the problem of issuing short-dated liabilities (e.g. demand deposits) whilst holding longer-dated assets (e.g. one-year car loans). There’s even a name for it: maturity transformation. It obviously relies on not all “depositors” wanting “their” money back at the same time and so is inherently unstable.

But it turns out we do have enough cash on hand. So we get to live another day.

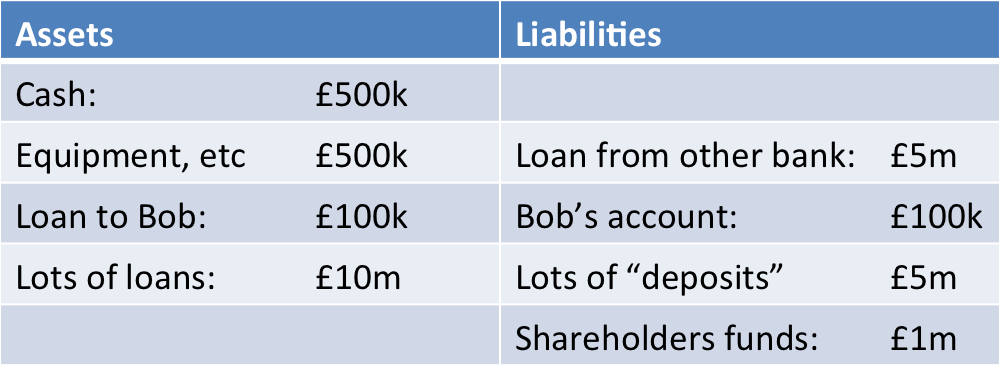

And this could go much further…. We could make lots of loans. As long as not everybody wants to take out money at once, maybe we’ll be OK. Let’s imagine lots of other customers plan to make some big purchases in the future and borrow some money from us. This is what the balance sheet would look like immediately after we’d made those loans but before any of them had withdrawn any of the cash:

We make lots of loans and make the balance sheet bigger and bigger…

What happens if the people who borrowed the money from us want to draw out the cash? They presumably borrowed the money for a reason, after all…

Well, that’s probably OK too, at least in “good times”. Let’s say they ask to withdraw £5m between them. There’s the minor problem that we don’t actually have £5m in cash… we only have £500k. But that’s OK… provided we’re not bust – that we’re solvent – and people believe we’re solvent, perhaps we can borrow the cash temporarily from somebody else – maybe the central bank.

So that’s what we could do:

We borrow £5m cash from somewhere else and use it to pay the depositors who want cash. Notice “deposits” have reduced by £5m and loans from other banks have increased by the same amount. The asset-side of the balance sheet is unchanged in this example.

Of course, another thing we could have done was sell some of the loans to somebody else for cash. And that would have also reduced the size of the balance sheet… since we’d only have £5m loans remaining on the asset side.

But it’s counterintuitive, isn’t it? We set up a bank that is making lots of loans and we’ve not yet taken a single deposit!

Indeed, it’s even weirder… we’ve created deposits seemingly out of thin air by the very act of making these loans. Where else did Bob’s “deposit” come from except from the fact that we made a loan to him? And it turns out this is a really important point. The Bank of England, no less, argues that this mechanism is the primary way money is created in the modern economy. Everything you were taught at school about how banks need to take in deposits in order to make loans isn’t actually true… But let’s leave that debate for another day…

“Deposits”

I once wrote a piece explaining how payment systems work. I was blown away by the response: hundreds of thousands of hits, huge numbers of them from people at banks. Clearly: this stuff isn’t as obvious as perhaps it should be.

One of the key points I made in that post was the one I was hinting at above: it makes no sense to say you’ve “paid money into the bank” or that you have “money at the bank”. There’s no jar in the back office containing your money, with your name on the front. Instead, when you “deposit” money with a bank, what you are actually doing is lending it to the bank. It ceases to be yours and that cash becomes an asset of the bank. It becomes theirs, to do with as they wish. In exchange, they make a promise to you: to give you cash in the future if you ask for it. You acquire a claim on the bank.

So let’s see how that works. What happens if and when somebody finally does make a deposit?

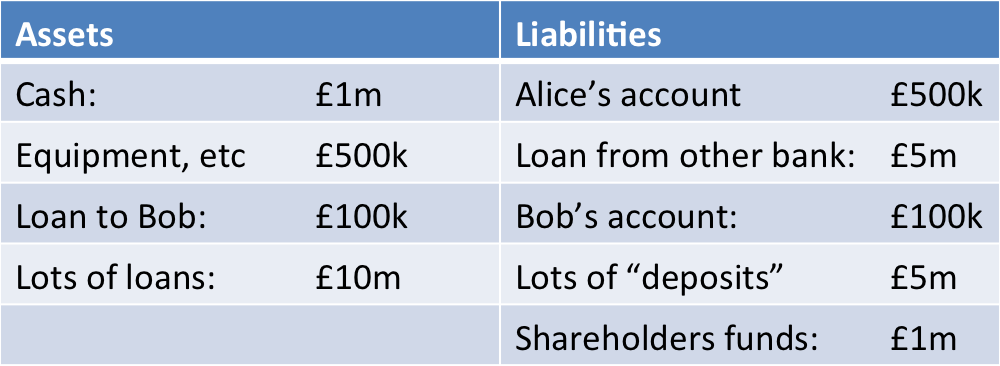

Let’s imagine Alice has just sold her house for £500k and needs somewhere to park the cash for a few days:

We have an extra £500k on hand as a result of a £500k deposit from Alice.

So this works as we’d expect: we record the fact that we owe £500k to Alice – our liability – and that we have an extra £500k in the vault (or with the Bank of England) – our asset.

OK, OK, Enough! What does this have to do with distributed ledgers?!

Well done for getting this far. Why have I written so many words and laboured so many points? Because, and as I argued recently, we could be moving to a world where agreements and obligations between firms are recorded on a shared ledger at the level of an industry or market, rather than on private systems maintained separately by each of the players.

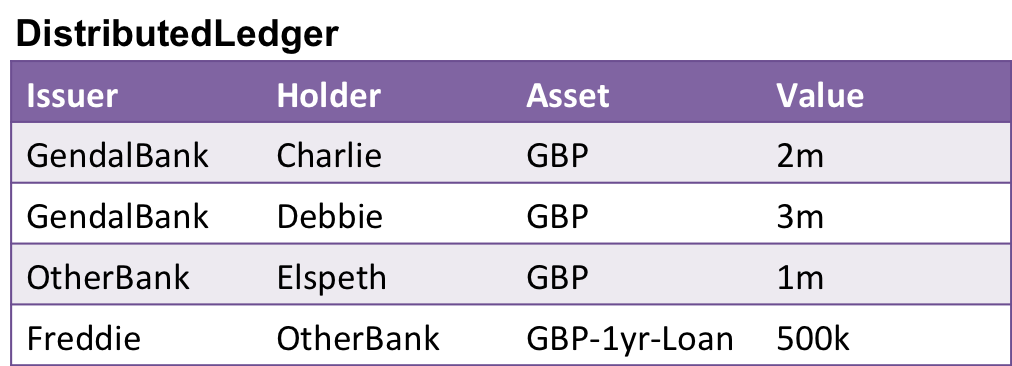

And, if this is true, we’re going to need to represent the idea that Alice has a £500k deposit at GendalBank or that Freddie has borrowed £500k from “OtherBank”. And this is only going to work if everybody building this systems has a deep, intuitive sense that “deposits” should be modelled as “claims against an identifiable entity” and that £500k at GendalBank is fundamentally different to £500k at OtherBank and so on. I think we need to be thinking in terms of a “four-column model” of “issuer”, “holder”, “assetID” and “quantity”:

Will the “four-column” model be the core data structure of the shared ledger world? (This is not an original idea to me: the concept is at the heart of systems like Ripple, Stellar and Hyperledger, amongst others)

Perhaps more importantly, once you start thinking about things in this way, it becomes possible to see the outlines of how the future state could work.

One can imagine a world where the bank still records that it owes some money to its customers but the shared ledger is the place that records precisely who those people are. This is fundamentally different to using the shared ledger as a mirror (or mirroring it to the bank’s own ledger) – it’s more akin to seeing the shared ledger as a partial subledger.

And it might perhaps be something that gets adopted to different degrees by different firms.

Perhaps GendalBank just uses the shared ledger to record some balances. So we update GendalBank’s system to say that it owes £5m to somebody but that it’s the distributed ledger that records to whom. And we see on the distributed ledger (above) that these people are Charlie and Debbie. So the total (£5m) is recorded in both places but only the shared ledger keeps track of the fine-grained detail. So it becomes a logical sub-ledger for some deposits (“DistLedger below) whilst the bank’s own ledger is used to record other facts.

Perhaps GendalBank only uses a shared ledger to record details of some accounts (“DistLedger”) and continues to maintain others locally.

OtherBank, by contrast, might go further and move pretty much everything to the distributed ledger – both records of its liabilities and assets. So OtherBank’s internal ledger is extraordinarily simple: it just records the value of assets and liabilities managed externally on the shared ledger:

OtherBank has “outsourced” or moved all processing to the shared ledger

So what?

Let’s look at the shared ledger again:

Imagine you’re Charlie. If you have the ability to read/write to this shared ledger, you could pay away your claim against GendalBank to any other user of that ledger without having to go through any of GendalBank’s systems. We’d have decoupled the deposit-taking and lending functions from the record-keeping, accounting, payment and trading systems.

If you were OtherBank, you could sell your loan to Freddie to somebody else and the business logic might move with the loan (the “smart contract idea): previously illiquid assets might become tradeable under this model. As I keep saying, this space is about more than just payments, after all.

Now, obviously: there is a lot of detail here that I’ve not even touched on. The reality is going to be so much more complex than this.

But hopefully this sketch shows some possibilities for where this could be going. And, like I said earlier, none of this will happen unless we get everybody to the same page with the right mental model for how banking works…

Appendix: Aside on Regulation… what stops us going completely mad with this?

I can’t write a piece on bank balance sheets without talking about risk. And a legitimate question is: if my analysis above about how loans are made and deposits are created is correct, what’s to stop us going completely mad and taking in huge amounts of deposits or making huge numbers of loans? Don’t irresponsible banks tend to get into trouble and need to be bailed out? Well, yes they do. And there are (at least) two very different things that can go wrong.

Illiquidity

The first problem banks can face is one of liquidity. Imagine lots of customers want their money back at once and the bank doesn’t actually have enough cash on hand. What happens?

As discussed above, the bank might be able temporarily to borrow the cash from somebody else. But what if nobody wants to lend it to the bank? They’d be suffering from illiquidity: the value of their assets exceeds their liabilities, so they’re not bust… but they can’t meet their obligations to repay people. Oops!

In most countries, the central bank will step in in such scenarios and temporarily lend the money to the banks. Indeed, we might say that the ECB’s “Emergency Liquidity Assistance” programme for Greek Banks was an example of this: on the assumption (pretence?) that the Greek banks weren’t bust, the ECB lent increasing amounts of Euros to the Greek banks to support deposit outflows.

From a regulatory perspective, rules such as the Basel Accord’s “Liquidity Coverage Ratio” is an attempt to force banks to hold enough cash (or cash-like instruments) on their balance sheet for forseeable withdrawals.

Insolvency

Another problem banks can run into is insolvency – being bust. It’s easy to see how this could happen:

Imagine that some of the people to whom you’ve lent money lose their jobs or their companies go bust and you suddenly realize there is no way they will ever be able to repay their debts to you.

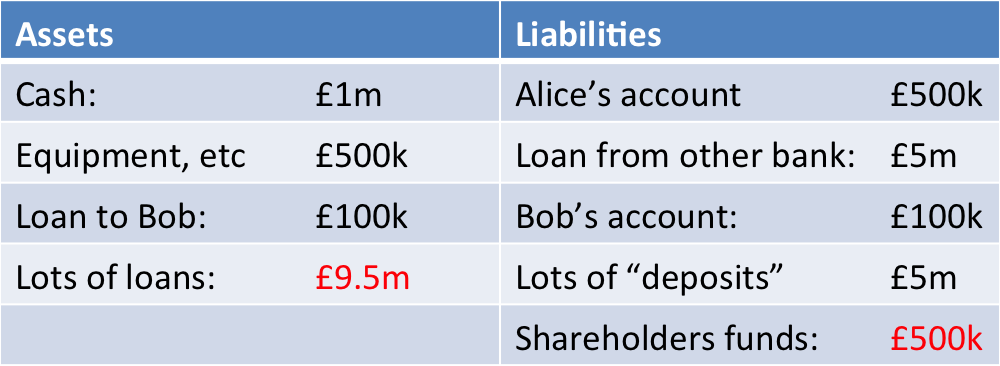

Let’s say £2m of the loans you’ve written become unrecoverable. So you “write down” the loan book from £10m to £8m… since you now know you’ll only ever recover £8m.

Now your assets are worth £9.6m. But your liabilities haven’t changed. You still owe £10.6m to your customers and the banks you’ve borrowed money from.

You owe more than you own. Game over. Good bye. You’re insolvent.

Your losses on loans mean your assets are now smaller than your liabilities. You’re bust

But notice something really interesting…. If you’d only lost £500k on your loans, you’d have been OK because your assets (£11.1m) would have still been greater than your liabilities (£10.6m):

… but if you only lost £500k on the loans you’d have been OK

So you can lose some money on your assets and be OK. But if you lose too much, you’re in trouble. What determines how much you can afford to lose? The answer is capital – shareholders’ funds.

You got away with the £500k loss but not the £2m loss because of your capital. Your shareholders took the hit. Before the bad debts came along, their residual claim on the company was worth £1m. A £500k loss takes their claim down to £500k. But in the £2m bad case above, the loss was greater than the “loss-abosrbing” cushion of £1m provided by the capital and that’s why you went bust.

And so this is why regulators are so fixated on capital: the more the bank is funded by capital rather than deposits or debt, the more resilient the bank is when they make losses on their assets. Capital can be written down to absorb losses on assets in a way that debt can’t. It’s why you hear so much talk about “capital ratios” and the like: what percentage of your assets should be financed by capital rather than debt?

But notice: the bank is in no sense “holding” capital. You hold assets and capital is not an asset… Instead, think in terms of capital being a mechanism through which the bank is funded.

And these phenomena can interact: if you are illiquid, you might need to sell lots of assets a “firesale” prices, turning a liquidity problem into a solvency problem.

[Update 2015-07-05 My description of insolvency is *very* simplified, as Ken Tindell has noted here… https://twitter.com/kentindell/status/617719608875872256]