I wrote a piece last month explaining how the payment card industry works. I talked about the various actors (acquirers, issuers, schemes, merchants, etc) and pointed out how weird it is that everybody knows the Mastercard and Visa brand names yet nobody actually has a relationship with them. One of the questions I didn’t address there was fees. Who makes all the money? Why does it seem so expensive?

Let’s start with the standard four-party model: Merchants, Acquirers, Issuers and Schemes:

The four-party model: Merchants obtain card processing services from Acquirers, who route transactions via Schemes to Issuers, who debit Consumers’ accounts.

- Acquirers are banks, but their services are usually provided by specialist acquirer processing firms such as Elavon, First Data, Global Payments, WorldPay

- Examples of schemes are: Visa Inc, Visa Europe (a different, although closely related, company), Mastercard, China Union Pay

- Issuers are banks and other card firms (e.g. Bank of America, Capital One, etc). They usually employ the services of specialist issuer processors such as TSYS.

- (And, of course, some firms are active in multiple categories.) In the UK, Barclaycard is a notable example of a firm which is both an issuer and an acquirer and which does its own processing.

A Worked Example

The key point is that one firm from each category is going to be involved in every payment card transaction. So it’s interesting to ask: how much do they get paid?

Let’s take a concrete example and work it through. Bear in mind: this is just an example. As you’ll see, there are almost infinite variations and some merchants will pay fees considerably higher than the ones I discuss below. Also, note: this information all comes from public sources. I use company names below for clarity but I have no private insight or information into their fee structures

The Scenario

Let’s imagine I’m using a Visa Debit card, issued by a US bank (let’s say Bank of America) to buy $100 of goods from an online retailer. What happens? From my perspective, of course, it’s obvious: I’m paying $100!

Imagine I am using my Visa Debit Card, issued by Bank of America to pay for $100 goods from an online retailer.

The Merchant’s Perspective: The Merchant Discount Fee

What does the merchant see? Well, the merchant will have a contract with an acquirer. What does that look like? Let’s take an example. Costco have a page on their website that refers small merchants to Elavon for acquiring services. Let’s use the pricing displayed on that page for Online transactions:

1.99% plus 25c per transaction (plus some other recurring/monthly fees, etc)

Many readers will be thinking that seems low but let’s go with it for now.

So, for our $100 transaction, we can calculate how much money the merchant will actually receive from Elavon/Costco:

- Transaction value: $100

- Elavon/Costco takes 1.99% + 25c = $2.24. This is often called the “merchant discount fee“

- So merchant gets $97.76

So our picture now looks like the one below:

Merchant receives $97.76 from the $100 transaction. Elavon gets $2.24. But how is the $2.24 distributed between the acquirer, issuer and scheme?

The Issuer’s Perspective: The Interchange Fee

So we know how much money the merchant has paid to the “credit card industry”. But how is that money allocated between all the participants? Visa Inc has a very helpful document on their website, which tells us part of the story: Visa U.S.A. Interchange Reimbursement Fees.

The key word here is “Interchange”. Interchange is the fee that gets paid to whoever issued the card – and it’s set by the scheme (Visa in this case). You’ll see in that document that this is not straightforward… there are pages and pages of rates: the interchange fees vary based on whether the card was present or not – and on the type of good or service being bought, whether it was a debit or credit card, whether it was a corporate card, whether it was an international transaction and lots of other criteria…

So let’s just pick a simple example. We’ll go with page 2 – “CPS/e-Commerce Basic, Debit” (Card not present).

Aside: CPS means that the merchant has complied with various Visa rules (such as validating customer address to reduce fraud risk, etc) and has thus qualified for a low cost option.

So the issuer is entitled to 1.65% + 15c

- Transaction value: $100

- Issuer receives 1.65% + 15c = $1.80. This is the interchange fee

- So issuer owes $98.20 to the other participants (Visa, Elavon and the Merchant)

And we already know that the merchant only gets $97.76 of that money (their merchant discount fee was $2.24, remember?). So that means there is 44c left to share between Visa and Elavon.

The diagram below shows the current state of the calculation:

Interchange Fee (what the issuer gets) is $1.80

So how is the remaining 44c allocated?

We’ve assumed the switch is Visa so we need to know much they charge. CardFellow.com has a good explanation.

We’ve assumed a Visa Debit card so, according to that site, Visa’s fee, which we call the “Assessment” is 0.11%. There is a menu of other charges that might apply but we’ve assumed this is a low-risk “CPS” transaction so we’ll assume none of them apply. (In reality, the 1.55c “Acquirer Processing Fee” probably applies)

- Transaction value: $100

- Visa assessment is 0.11% so Visa charges 11c.

- So there is $98.09 to pass on to the acquirer.

And if there is $98.09 to pass on to the acquirer and we know that the merchant receives $97.76, that must mean there is 33c left for Elavon.

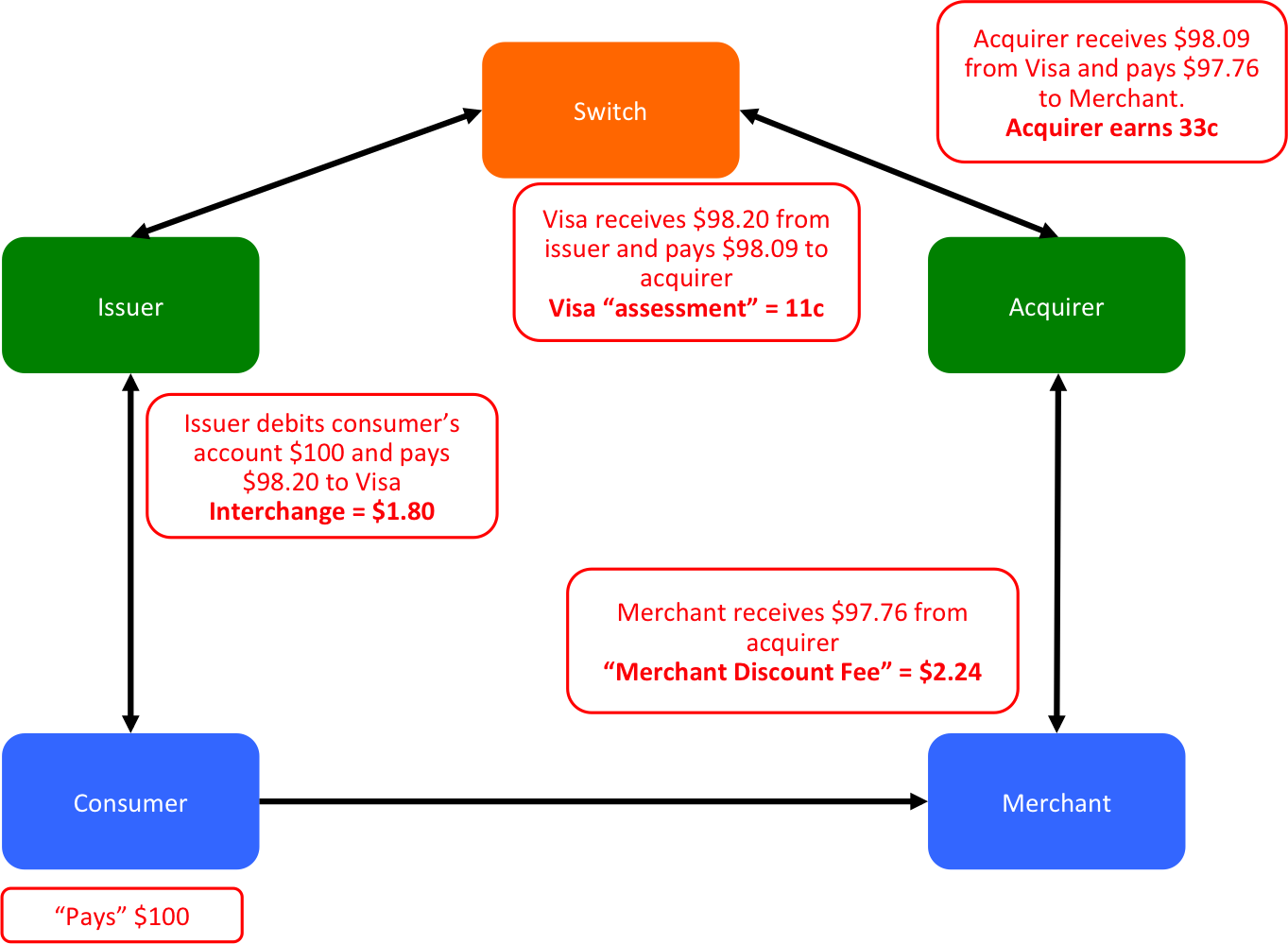

So there we have it… in this VERY SIMPLE, highly contrived – and probably unrepresentative – example, we end up with the result in the diagram below:

- Consumer pays $100

- Issuer receives $1.80

- Visa receives $0.11

- Acquirer receives $0.33

- Merchant receives $97.76 – overall fee $2.24

Final picture showing how the merchant’s $2.24 fee is allocated

As I’ve stressed above, this is just a simple example but it shows two key points:

1) It is the issuer who receives the bulk of the fees (this is, in part, how they fund their loyalty schemes, etc)

2) The schemes actually earn the least, per transaction, of any of the participants. This underlines, again, how powerful their business model is: by being at the centre of a very sticky network, they can earn a lot of money overall by charging very low per-transaction fees. [Edit 2013-08-10 10:35 : it’s also worth noting that the acquirers and schemes have pretty much fixed-cost infrastructures – unlike issuers, who need to hire customer service and debt collection staff in proportion to number of cards issued. So the schemes and acquirers also benefit disproportionately from rising volumes. So: low fees for schemes/acquirers for sure… but HUGE volume is what enables them to make big profits]

[Note: I use blog posts like this to help clarify my own thinking and understanding – as well as to share knowledge… and there are one or two pieces here where I’m not 100% confident I got it totally correct… so please do tell me where I’m wrong if you spot something]

[Update 2014-08-09 18:47 Minor typos and replaced last diagram]