Just when I think I understand the cryptocurrency/block chain space, I realize I didn’t understand anything at all

Four recent events have made me realize that I don’t understand this space anywhere near as well as I thought I did. But that’s good: it means I’ve been forced to come up with a new mental model to explain to myself how all these projects relate to each other.

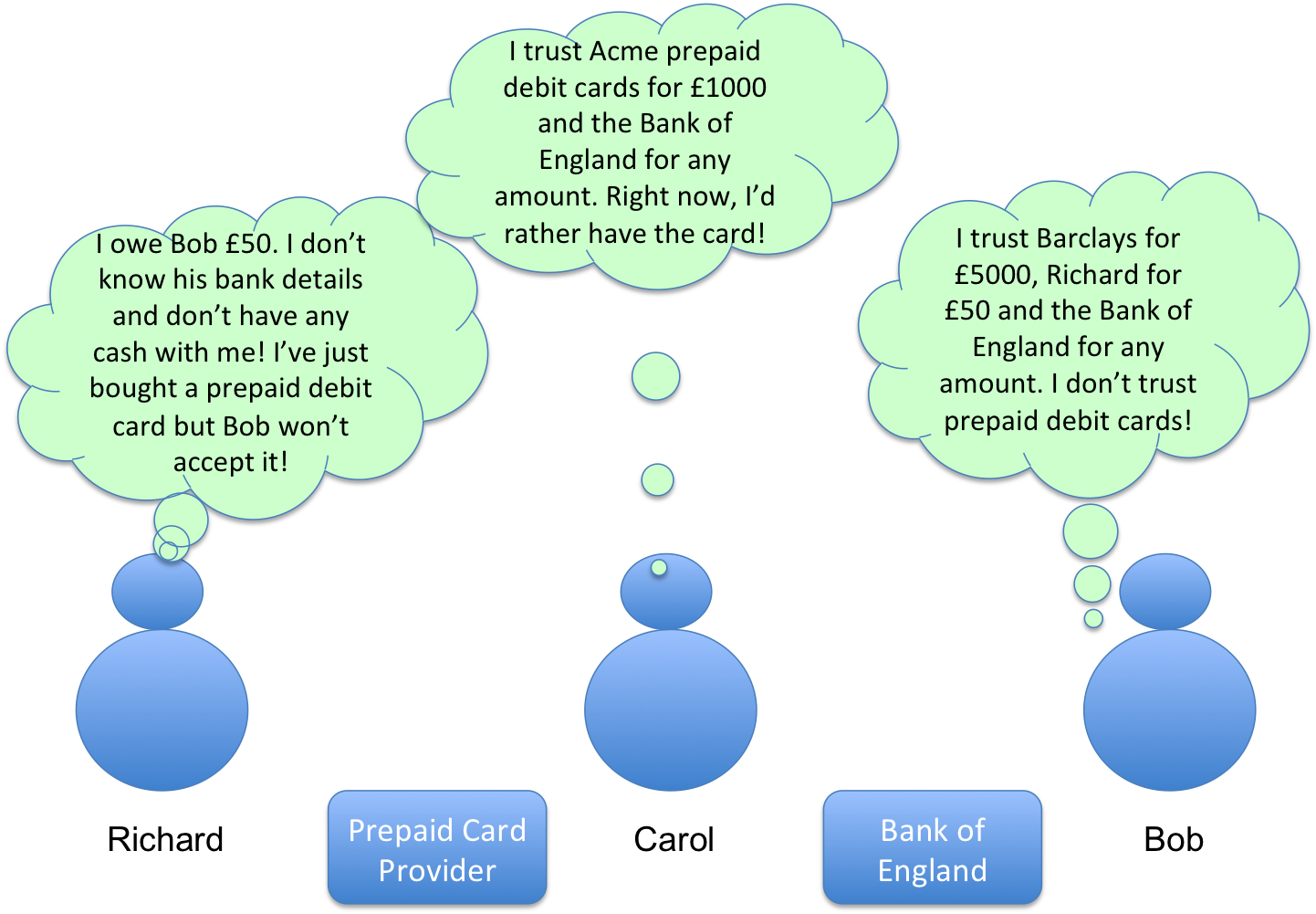

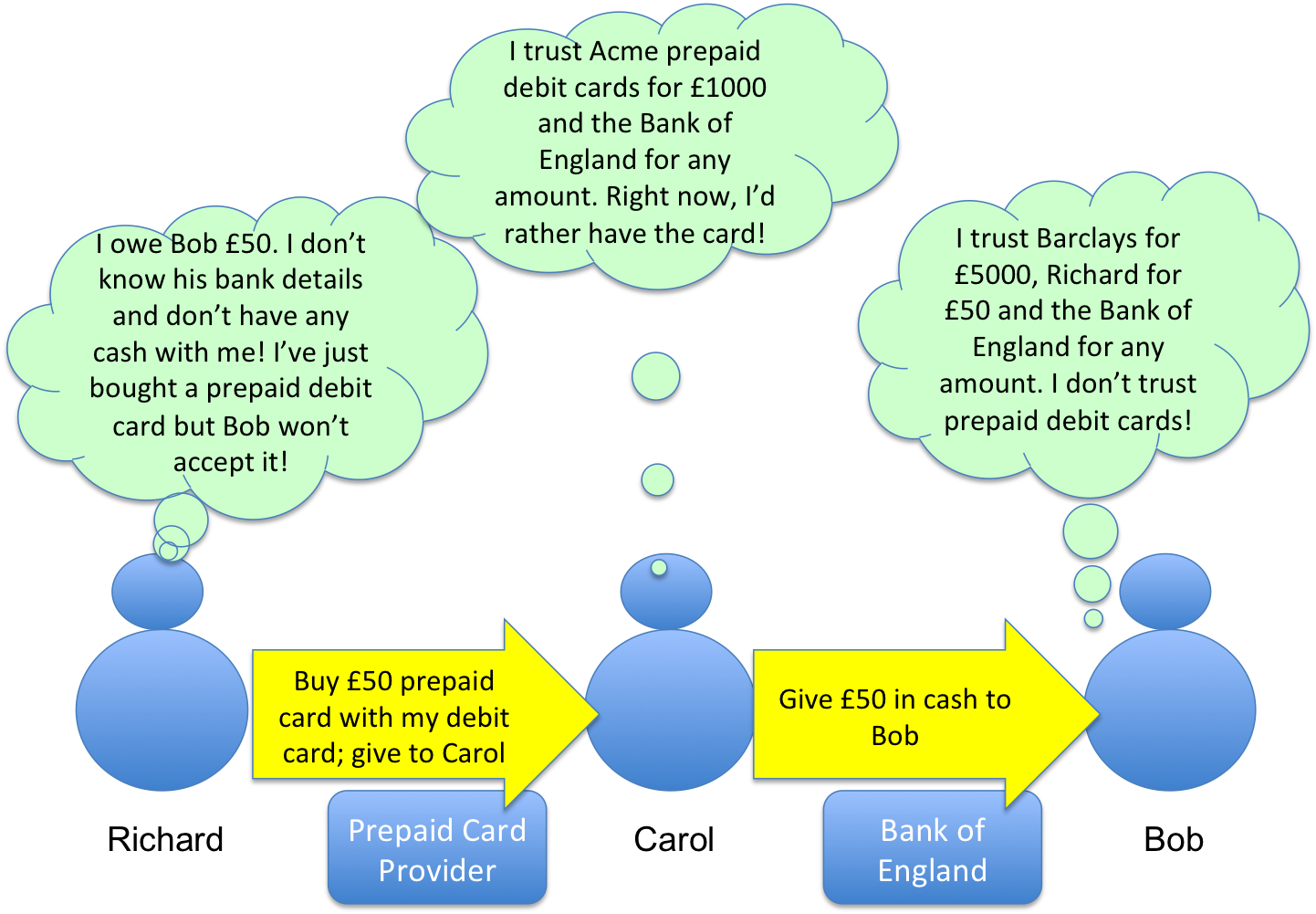

TL;DR: the two questions to ask about a “fiduciary code” requirement are: who do I need to trust and what am I trusting them about?

A simple model to capture the essential differences between some consensus platforms

The rest of this article describes the four events that influenced me to draw it.

Event 1: Nick Szabo’s “The Dawn of Trustworthy Computing” Article

In his recent article, Nick Szabo introduces two really helpful terms to explain what makes systems like Bitcoin particularly noteworthy.

- First, he talks about “block chain computers”. He defines these as the combination of the Bitcoin consensus protocol and strong cryptography to create the unforgeable chain of evidence for all data stored in the block chain data structure. I think this formulation is useful because it shines a bright light on an obvious, but often overlooked fact: a “block chain” is just a data structure, utterly useless on its own. What makes the Bitcoin blockchain remarkable is the network of computers – and protocol they follow – that makes it so hard for any single actor, no matter how determined, to subvert it.

- Secondly, he talks about “fiduciary code”: the code in an application that needs to be the most reliable and secure. For example, in a banking application, this is likely to be the core ledger: who owns what. He points out that a secure block chain computer is an extremely expensive piece of kit: you should only use it to secure that information that really needs it.

Event 2: Albert Wenger’s “Bitcoin: Clarifying the Foundational Innovation of the Blockchain” Article.

In this piece, Albert Wenger makes a really obvious-in-hindsight point: Bitcoin-like block chains are organizationally-decentralised – no one organization can control it but the entire point of the system is to build and maintain a logically-centralised outcome: a single copy of the ledger, which everybody agrees is the true single copy.

ArthurB uses the term “decentralized mutable singleton” to capture the same idea, I think.

And he echoes one of Szabo’s implicit points: a “block chain” is not something of value in and of itself. This insight is also important because it edges us further away from the idea that “decentralization” is some sort of end-goal or absolute target. I made a similar point in this piece on the “unbundling of trust” but Albert and Arthur have captured the key point far more succinctly.

Event 3: The Eris Launch

On Wednesday this week, Eris Industries held the launch event for their new platform. Tim Swanson has done a good job summarizing the Eris concepts. (Disclosure: I was invited to, and attended, the launch).

I’ll admit I still don’t fully understand it. But the general picture that’s forming for me is of a platform that allows you to build and maintain one of these “decentralized mutable singletons” but to specify precisely who is allowed to update it and under what conditions.

In essence: take the idea of a shared common state (Albert’s Arthur’s “mutable singleton”) but relax the constraint that the maintenance of it necessarily happens in a fully public, adversarial environment, for which something like a proof-of-work system may be required, and allow for the idea that the participants might be known. [EDIT wrong name!]

Fine… but I think the Eris insight is where they go next. They suggest that if you had such a system then you might also be able to distribute the processing of application logic more broadly, too. And I think it’s the application logic they’re most interested in. Their documentation is full of talk of “smart contracts” and it’s perhaps no surprise that their founders are lawyers. In fact, maybe that’s why I don’t understand it as well as I’d like: lawyers just seem to speak differently. Maybe I need a translator.

And to be clear, the part I don’t fully understand just yet is why you need a “block chain” as the underlying data structure in this model, rather than something based on more general-purpose replicated database technology. But this may turn out just to be an implementation detail: so let’s see how they get on over time. There seems to be a lot of content, reflective of a lot of thought, on the various Eris sites.

Event 4: I looked at HyperLedger in more detail

I had reason to look at HyperLedger this week and, combined with my study of Eris, it was this event that finally convinced me that my mental model of this space was far too simplistic.

Hyperledger calls itself an “open-source, decentralized protocol for the recording and transferring anything of value”. This is a bit like how I might have described Colored Coins or Ripple to people in the past.

But what makes Hyperledger different is that they allow the creation of multiple ledgers (one per asset per issuer) and each ledger can be configured to have different consensus rules – you don’t have to make the assumption of an adversarial open public environment… so some similar assumptions to Eris here, but with a ledger designed to track assets rather than business logic/contracts.

Where is this heading?

So I spent some time this evening trying to piece all of this together in my brain.

I’m pretty sure these projects all sit in Szabo’s “Fiduciary Code” space: they only really have value or make sense if the facts they’re recording are really important!

But they make different assumptions about the threat model they face – and some of these assumptions are very different to the ones against which Bitcoin was designed. And they’re different to the assumptions underpinning some other prominent platforms, such as Ripple, which, through its use of validators and “Unique Node Lists” has a model, whereby you trust a set of known entities who, in turn, trust some other entities, and so on.

In addition, the facts these systems are recording are very different: ownership of a real-world asset on Hyperledger is different to ownership of a bitcoin on the Bitcoin ledger; a ledger-native asset has no counterparty risk, whereas a real-world asset needs an identifiable issuer. And they’re both different to a platform that potentially executes legal contracts.

So I tried to think of dimensions along which you might be able to classify these projects… and I came up with too many.

But it’s almost Christmas and I’m not to be deterred! Is it really too much to ask for a model with just two dimensions, that doesn’t require a 3-D screen to render?! So I kept on going. And, finally, came up with something that looks so trivial, I worry it may be content free. But here it is anyway.

I think the two dimensions that help me think about these projects are:

- “Who do I trust to maintain a truthful record?”; and

- “What do I need the record to be about”?

Here is the model I came up with. It’s obviously not complete and you could put some projects in multiple boxes… but I think it captures the key distinctions.

Another way to think about the increasingly confusing cryptocurrency/Block Chain space

But this is just a view. I’d really value comments… especially if I’ve missed something really obvious.

[UPDATE 2015-01-08 DISCLOSURE: Since publishing this post, I have become an advisor to HyperLedger, in a personal capacity]