Nasdaq’s recent announcement shows you need a strategy for both

I have argued for some time that the world of “blockchains” is actually two worlds: the permissionless world of “bitcoin-like systems” and the permissioned world of “ripple-like systems”. The reason we so often talk about them together is because they share a common architecture: the “replicated, shared ledger”.

But they solve very different problems. Tim Swanson has written about the permissioned-ledger world and my last post gave an argument for why banks, in particular, should be paying close attention to them.

But this observation can be dangerous if people believe they are building a “blockchain strategy” for their firms when they are actually focusing only on the permissioned world.

As this exchange between Jerry Brito of Coin Center and Michael Casey of the Wall Street Journal shows, Nasdaq’s recent announcement of a blockchain experiment is noteworthy because they are explicitly building on Bitcoin, using a colored coins protocol, not on one of the permissioned/closed ledgers:

Forget Bitcoin at your peril?

As I argued in my last post, the world of permissioned ledgers is pretty easy to think about: if you’re in a market where multiple firms in the industry are all building and maintaining undifferentiated systems that do pretty much the same thing – and they have to be reconciled with each other – then it can make sense to replace them with a single system that you all share. But if you’re concerned about having a single central operator then these new blockchain technologies give you an option that didn’t previously exist: you can implement the common infrastructure on a replicated, shared platform that you all help secure/maintain and so mutualise the effort of maintenance rather than delegating it to a separate entity.

But, all too often, the analysis starts and ends there and disregards the “bitcoin-like” world. To see why this could be dangerous, we need to go back to the beginning.

The first nine words of the abstract to the Bitcoin whitepaper tell you everything you need to know to understand its architecture:

Everything you need to know to understand Bitcoin

“A purely peer-to-peer version of electronic cash”

Those nine words seem innocuous but they have profound implications and explain why so many people still steer quite clear of it. The key is “electronic cash”. What can you do with cash that you’d need to emulate in an electronic version?

- First, cash is a bearer asset. The only way somebody can take away the money in my pocket is by confiscating it from me. Nobody in a central bank can “delete” my cash whilst leaving everybody else’s untouched.

- Secondly, cash is a peer-to-peer instrument: I can pay you directly. There are no third parties we need to rely on, assuming we’re physically co-located

There’s a phrase for this set of requirements: censorship resistance. A true system of digital cash can only work if it is censorship resistant. And Bitcoin’s architecture does a pretty good job of achieving this through a very novel architecture. I sketch out some of the details for interested readers at the end of this article.

There’s just one tiny problem…

Censorship resistance is not an objective that is shared by most governments, regulators, banks or most individuals! No wonder there is so much controversy around the system. Perhaps it’s just easier for respectable firms to steer well clear.

And it gets worse when one observes that Bitcoin is worse than existing digital money in pretty much every significant way! It’s slower, it’s more expensive to operate, its value jumps all over the place and it’s really hard for consumers to use safely. So ignoring it is perfectly understandable.

But it could also be a mistake.

Permissionless Innovation

Because it turns out that censorship-resistance implies an even more interesting property: permissionless innovation.

“Permissionless innovation”—the general freedom to experiment with new technologies and business models—has been the secret sauce that fueled the success of the Internet and the digital economy

Think back to the design goal for the bitcoin system: electronic cash. And how that implied a need for a censorship-resistant bearer asset. These scary properties from a regulatory and banking perspective imply some very interesting properties from a technical perspective: this is the world’s first asset that can be held by anybody or anything and transferred to anybody or anything without needing permission.

Why could that be interesting? Let me sketch three simple scenarios:

The Internet of Things

How do you do KYC on a fridge? Do you really want your washing machine having your credit card details on file? Perhaps the future of machine-to-machine payments is one where the machines hold their own assets on an open system. Sure: you could build a permissioned payments system for device-to-device payments but the simplicity and open-access nature of Bitcoin could mean that it’s just easier to do it that way.

Firms for whom payments are a secondary concern

We often make the mistake of viewing this space through the eyes of incumbents. It can be useful to put ourselves in the shoes of others. For example, imagine you’re building a business for which getting a bank account and payment processing services would be difficult. Maybe you plan to operate in tens of countries. Or perhaps payments are a secondary concern for one of your use-cases… you just need a quick and easy way to make and receive payments. Sure… you could go through the process of getting a merchant account, signing up with a payment processor, proving compliance with various security standards. Or you could just use something with no barrier to adoption: bitcoin may have lots of problems but at least you can be up and running in seconds.

Second-order use-cases

Perhaps the most interesting future scenario is one where bitcoin isn’t used for payments at all. Instead, the security and censorship-resistance of its platform is seen as having value in and of itself – perhaps for notary services in the first instance – recording facts about the outside world – and so Bitcoin becomes nothing more than the token you need to own in order to purchase the services of the network. It becomes an app-coin, if you like.

Why we need to keep an eye on the Bitcoin world

I accept that none of these use-cases is particularly compelling as I write this piece. There are lots of great counterarguments for all of them. But that’s partly the point: if any of these were obvious, nobody would be dismissing it.

And this is why I find the Nasdaq example so interesting. Using the inherent security and open-access of the Bitcoin system to “carry” representations of real-world assets – “colored coins” – is an old idea*. And it also fits into my “second-order use case” category above.

Now, Tim Swanson and others have written convincingly about many theoretical issues with the idea but we now have a brand-name firm experimenting for real and we’ll hopefully all learn from the exercise in time.

So, sure: bitcoin raises all kinds of conceptual, legal, technical and philosophical questions. But it would only take one of these scenarios to drive some adoption and, very quickly, bitcoin might cease to be a sideshow. And, given that its core design goal of censorship-resistant digital cash has such disruptive potential – good and bad, this possibility alone is reason to keep an eye on it. Dismissing it entirely could be a big mistake.

Coda: How to build a system of digital cash

Note: you don’t need to read this section to understand the main argument of this piece.

Recall the implications of a true digital cash system: censorship resistance. This drives some very strong implications for anybody trying to design such a system:

First, you simply can’t have the concept of an issuer in such a system: the issuer could selectively choose to honour only certain claims.

So, if you can’t have an issuer of the currency on such a platform, it will have to be native to the platform. Hence Bitcoin as the currency unit and the interminable debates about why it has value and what that value should be, if anything.

If you want true electronic cash, there can’t be an issuer. So the asset has to be native to the platform

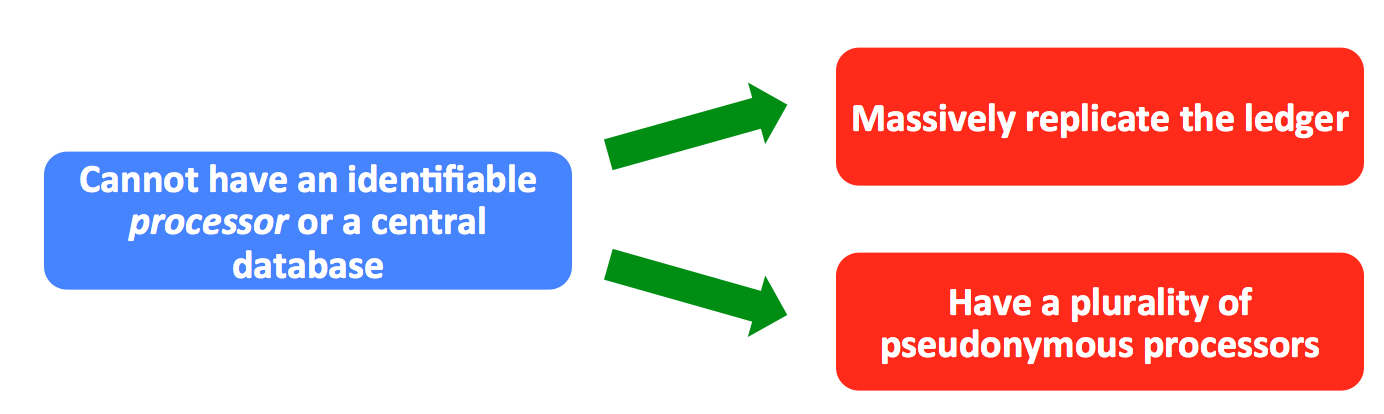

Secondly, you can’t have an identifiable operator or processor for such a system, either: they could choose to block certain transactions and their central database would be an obvious target for those seeking to exert control. So this means you need to have lots of actors providing the processing services and they need to be able to join and leave. And they probably also all need their own copies of the ledger – we can’t have a single central one, after all:

If you want true electronic cash, its ledger will have to be massively replicated and you’ll need a large pool of “processors”

Thirdly, you’ll need to pay the processors. You obviously can’t pay them with “real” money (since the issuer of that money could simply refuse to allow payments to be made to processors who refuse to co-operate with them). So you’ll need to pay the processors with the platform’s own asset:

If you want true electronic cash, the processors will need to be paid in the currency of that platform.

The breakthrough of bitcoin was figuring out how to put these building blocks together: how to ensure sufficient scarcity of the currency unit? How to keep the multiple ledgers synchronized? How to ensure the processors’ incentives are aligned with those of the users of the system? And so on.

There’s more than one way to talk about it

Of course, this isn’t the only way to think about the system. If you’re still interested, here’s my attempt to explain how it works by imagining how you could invent digital cash using an email system.

*Disclosure: I am an adviser to a colored coins firm (ChromaWay) in a personal capacity, albeit one that uses a different architecture to the one apparently being explored by Nasdaq