Decentralization and centralization are two ends of a continuum. Look for opportunities to disaggregate “bundles of trust” to identify good opportunities in the cryptocurrency space

There are so many potential uses for cryptocurrency technology. But how do you know if any of them are good ideas? Blockchain-mediated financial exchange? I have a good feeling about that one. A bank-sponsored local currency system for small businesses? My sense is that it’s probably a terrible idea. But short of going out and building it, how would you know?

So are there any test you can apply beforehand to figure out if a blockchain is a good technical solution for a given problem? And can you turn a bad idea into a good idea?

It’s a topic that comes up regularly when I present to audiences on Bitcoin and cryptocurrencies. Here are some slides I often use in these discussions. Slide 15 is where I discuss this topic.

Slides I sometimes show when presenting on cryptocurrencies. These represent my views, not IBM’s. But they are Copyright IBM. Please do not reproduce without asking permission first.

For me, the key to deciding if an idea is good enough is the one I’ve summarized on page 15 of the deck: this space is all about decentralization and if your problem isn’t about centralization then this technology may not be for you.

That may sound obvious. But internalizing this point is the key to understanding what a good cryptocurrency use-case looks like. And how to turn a bad one into a good one. Because even if your problem looks centralised, there may be portions that don’t need centralised trust and unbundling those components could be the key to doing something valuable. Here’s what I mean…

Go back to the beginning: what problem was Bitcoin designed to solve?

Bitcoin was invented as an answer to a decades-old question:

How do you come to consensus about some facts with a large group of people when you don’t know each other and some of you are cheating?

In Bitcoin’s case, the “facts” are “who owns what?”

And one answer to that question is, of course: “we all agree to trust somebody (e.g. a bank) and now we don’t need to trust each other”. But the obvious problem is: you have to trust the bank and that’s a potential point of failure. The breakthrough of Bitcoin was in showing us how to answer this question in a way that doesn’t require us to trust any single third parties.

We say the system is “decentralized”, as a shorthand for this concept.

(As an aside, I explained Bitcoin from first principles in this post on how the counter-intuitive genius of Bitcoin is that it works by going slow! For those who want to go even deeper, I share a way to think about the confusing “Unspent Transaction Output” concept in Bitcoin through an analogy of land.)This is why Bitcoin is often positioned as being a decentralized equivalent to the centralized banking system:

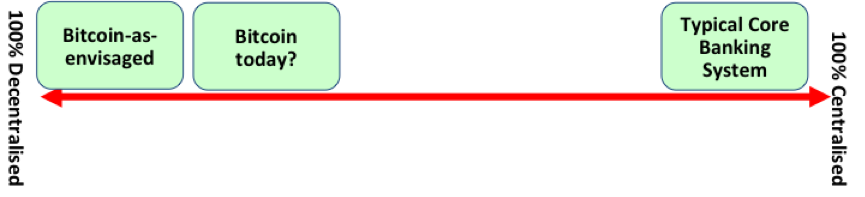

Bitcoin allows us to agree who owns what without having to know each other or trust anybody else. This is the opposite of the traditional system where everybody has to trust their bank

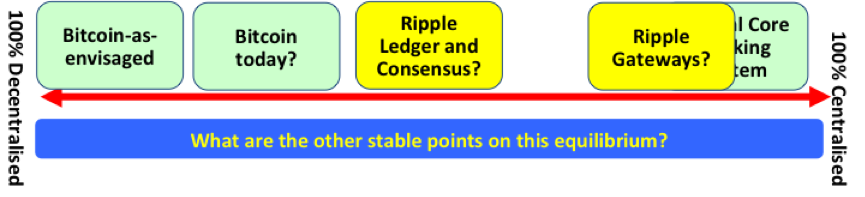

Bitcoin-as-envisaged isn’t what we have

But there’s a problem: Bitcoin-as-envisaged isn’t what we have today. Phenomena such as mining centralization and the use of SPV Wallets mean that Bitcoin isn’t completely decentralized. It’s not currently a problem but one can already see its effects. For example, some miners refuse to mine certain types of transactions. The effect on average confirmation time for these transaction types might be marginal but it exists, nevertheless.

So Bitcoin-today is somewhere in between. It’s not 100% decentralised yet nor is it centralized.

Bitcoin today is neither fully decentralized nor is it centralised

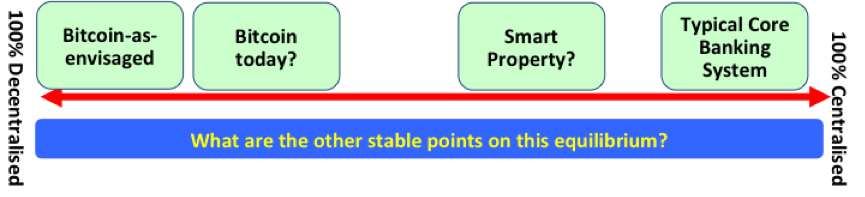

So it seems reasonable to consider that centralization may actually be a continuum rather than an either/or phenomenon:

Are centralization and decentralization actually two ends of a continuum?

This way of thinking can be helpful because it allows us to think about other innovations in this space, such as Smart Property.

Smart Property

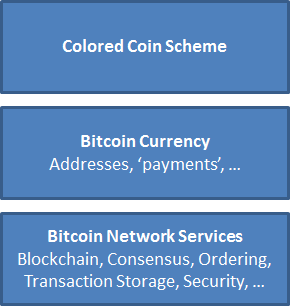

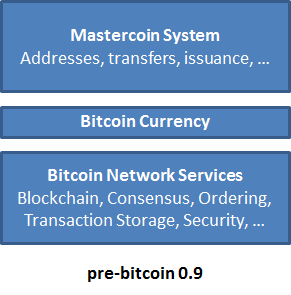

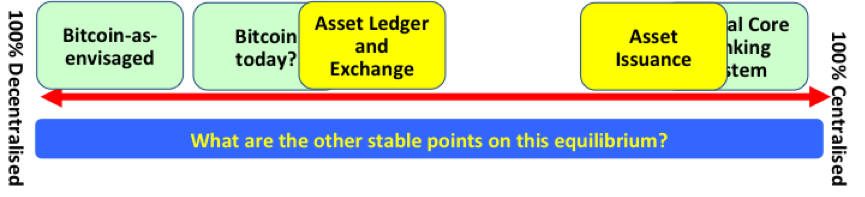

I’ve written in the past about a decentralized securities systems being built “hidden in plain sight”. The key idea here is that you can use blockchain platforms (like colored coins or counterparty, etc) to track the ownership and transfer of real-world assets. What distinguishes these platforms from Bitcoin itself is that they have to bridge to the real world: the asset could be a bond with a corporate issuer, being kept safe by a custodian bank, for example. So there are several real-world entities on whom you depend.

I’ve written about how smart property allows these two roles to be merged (the issuing company could do both) but somebody has to do it – let’s just call them issuers.

So this system has points of centralization (the issuers) and points of decentralization (the ownership tracking and exchange). So perhaps it sits somewhere here on the continuum:

Perhaps there is value in different “degrees” of decentralization for different business problems

You can have more than one type of decentralization in a single service

But it’s actually more interesting than that. Because not only do smart property systems sit somewhere on the decentralization continuum, the key point is that different parts of the systems sit in different places:

- the ledger, exchange and transfer system use the underlying Bitcoin consensus system – so they’re all pretty decentralized. No need to depend on any trusted third parties.

- But you do, of course, have to trust the issuer. That part of the proposition is centralised

So the important thing about smart property systems is that the all-or-nothing “trust bundle” is unbundled: you need to trust a specific issuer but the ledger, exchange and transfer functions are decentralized in their operation.

The unubundling of trust

And I think that’s what gives decentralised consensus systems some of their power: you can now break down products and services into their constituent elements of trust and implement each one with the most appropriate degree of centralization. For smart property, perhaps the picture looks something like this:

Different degrees of decentralization can exist within the same service: trust is being unbundled

So what?

Of course, none of this tells us whether smart property or cryptofinance is a good idea. But it is a way to think about whether a particular service is doing anything particularly novel. Think about it the other way: if somebody proposes a cryptocurrency business idea that doesn’t meaningfully unbundle any trust in an existing service, is it actually doing anything valuable? Likewise, take any real-world centralised service and ask yourself: what are all the things I need to trust for this to work? Which components have to be centralised? Which could be decentralised? Does that lead to lower risk? Lower cost? More opportunities for competition? Reduced friction for consumers? If the answer is “yes” to those questions then you could have an interesting proposition on your hands.

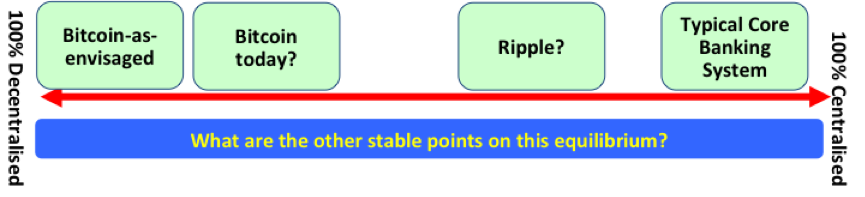

Unbundling trust in payments

A similar analysis works for systems like Ripple. Ripple’s architecture is more distributed than the traditional payments systems but less so than Bitcoin (at least as envisaged) so perhaps we may place it somewhere like this on the scale:

Ripple is another example of a “trust unbundling”

But, just like in the Smart Property example above, in the Ripple system there is a “trust unbundling” going on: the ledger is fairly decentralized in its operation whilst you necessarily need to trust a specific gateway. So it actually looks like this:

Different degrees of decentralization can exist within the same service: trust is being unbundled

To see why this is important, recall how current payment systems work. I wrote a simple explanation of it here. As the article shows, you have to trust a lot of moving actors and the point is that you have to take this as a bundle… it’s all or nothing. You trust all those parts of the system or you can’t achieve your objective. With a Ripple-like system, you only trust the minimal set of actors you have to – namely, the banks who issued liabilities. Everything else can be decentralised to some degree.

Unbundling trust in contract execution

One last example: a similar argument applies to financial contracts. Projects like Ethereum (and Counterparty!) are exploring the decentralized modeling and execution of law. Gavin Andresen has written about how something similar could be achieved on the base Bitcoin platform.

You can think of this in terms of “trust unbundling” too: the decentralized platform ensures the integrity of contract execution and you can use n-of-m oracles to provide reliable external data. You only trust who you have to, to the minimal degree possible.

Using “trust unbundling” to turn bad ideas into good ideas..?

So now we can put this model to the test. Does it help us spot the silly ideas? Even better, does it help us turn the silly ideas into good ideas? [UPDATE 2014-11-15 this section was heavily reworked)

Antonis Polemitis commented on an earlier version of this article:

Here’s what I think he means:

A better airline miles system?

As Antonis points out, airline miles systems are highly centralised: the airline is the issuer, redeemer, owner of the ledger, setter of the rules and controls everything else too.

So imagine an airline were to announce that their new airmiles programme was to be based on a fork of Bitcoin. Perhaps they would create their own Blockchain, issue the miles on top, secure it themselves and distribute wallets to all their customers. Brilliant… an airline miles programme with all the benefits of Bitcoin!

Really? From a consumer perspective, surely this system would be indistinguishable from a traditional system and what is the argument that says it would be better in any meaningful way?

But take a step back and think about airline miles again and think about the trust bundle. Which parts of the system require you to trust the airline? Issuance and redemption of the miles, for sure. And setting of the scheme rules. But storage, exchange and trade doesn’t need to be done by them.

And perhaps there’s a cost saving for airlines if they offload that work to a decentralised network and a benefit for customers if it gives them additional utility – perhaps new ways of swapping miles between competing programmes to accumulate enough points to book a flight? Some very interesting possibilities emerge if multiple airlines base their systems on the same platform or if third parties can build new services on top of a platform like this.

Suddenly you might have something interesting: an interoperable, multi-provider airline miles storage, transfer and redemption platform. Now it could be a terrible idea – these schemes only work because most miles are never redeemed, after all! But the thought process is important: who are users expected to trust to use your service? And what are they trusting them for? What if a component was decentralised? What new possibilities would that enable? What risk could it mitigate?

Now the real world is more complicated than this. But the key insight remains:

- if your cryptocurrency idea requires users to trust only you, you’re missing the point

- but if there’s something in the value proposition that can be usefully decentralized or shared with others, you could be on to something