Look beyond currency to see the true potential for cryptocurrencies… but don’t forget to apply the lessons to today’s problems too…

I participated in the Bitcoin panel at Finextra’s Future Money conference at Canary Wharf’s Level 39 in London this week. Zilvinas Bareisis of Celent has a succinct write-up of the event here. It was live-scribed by the amazing Mela Atanassova:

The Finextra team assembled the “who’s who” of the London FinTech scene and it pays to be prepared when speaking in front of that sort of audience… so I gave some thought to my talking points beforehand.

When I reflected on the event afterwards, it struck me that our moderator, Liz Lumley, had expertly led us through most of the key “what Bankers need to know” questions: In what way is Bitcoin different to what went before? Why do cryptocurrencies cause such intense discussion? Why do sensible people get so excited by this stuff? Where might it be going?

So in this blogpost I’ve combined my talking points with observations made by my co-panellists: Stan Stalnaker, Ali Farid Khwaja and Nadav Rosenberg.

How do you bring a diverse audience “up to speed” on Bitcoin?

Elizabeth Lumley kicked off the panel by asking who in the audience had a Bitcoin wallet. Over half of the hands went up. Oh dear… this was not your typical audience. What could we tell these people that they didn’t already know?

Luckily, we had been preceded by a keynote by Allessandro Hatami of Lloyds Banking Group. He’s a very smart guy and he gave a thought-provoking presentation. But I noticed something interesting: although he only mentioned Bitcoin in passing, he referred to it in the same context as Amazon Coins. Now, I’m sure he understands the differences but it highlighted that it’s very easy to lead audiences into “category errors” if we’re not careful.

Luckily, we had planned for this in advance. So I spent a few minutes outlining what I think is the “irreducible core” – or fundamental difference – of cryptocurrencies relative to everything that went before, using my “how I explain Bitcoin to new audiences” piece as the structure.

In short:

- Bitcoin is audacious: until cryptocurrencies came along, humanity had no ability to transmit value at a distance without the permission and support of a third party. Bitcoin taught us how to do it.

- Blockchain technology could be as important as the web: if we think of the web as the world’s first “internet-scale open platform for information exchange”, we can think of the blockchain as the world’s first “internet-scale open platform for value-exchange”. And the openness is the key.

- The implications go beyond payments: think “economy of things” and “smart contracts”

In other words, if you’re thinking Bitcoin means “funny internet money”, you’re missing the point.

OK – it could be a cool piece of computer science. But why are so many serious people talking about it so seriously?

Some very smart, very sensible people have concluded that the “web analogy” is plausible and are investing and working on that basis. Other people have been transfixed by the elegance of the underlying consensus algorithm. So it’s not surprising that Bitcoin has unleashed a storm of commentary.

But I think there’s also another reason. I think that Bitcoin has made large numbers of intelligent, thoughtful people realize that they didn’t understand the things they thought they understood. And they are rather enjoying the intellectual rabbit-hole of discovery it has sent them down as they try to “re-learn” things they thought they already knew… This is certainly the case for me. It makes us think deeply about questions like:

- How does today’s payment system work?

- What is the difference between a push and pull payments?

- How are securities trades settled?

- What is money? [Sorry… couldn’t resist this link]

The eye-opener for me was what happened when I published my piece on how payment systems work. I wrote it for Bitcoin users who didn’t know much about the banking system. What surprised me was who read it. It was being linked to from banks’ own internal training sites. The answers to these questions are not obvious and Bitcoin has inspired many of us to really think about them.

And I believe this is a big reason why so many people are talking about cryptocurrencies: they force us to clarify our own thoughts about things we thought we already knew.

OK – so cryptocurrencies are important and have potential. But give me just one good example of how it’s going to replace what we already have

I was challenged by a banker in the audience who had clearly heard the cryptocurrency story several times before and was growing tired of all the hype. Sure – it’s clever. Sure – it lets us do things we couldn’t do before. But so what? What real-world problem does it actually solve?

I answered this in three parts.

First, I pointed out how there is a short-term opportunity to take huge cost out of International Remittances. Not glamorous but a clear area where the technology could make a difference to the world.

Second, I argued Bitcoin helps us think about value: what makes today’s financial institutions valuable? Consider Payment Cards. If Bitcoin allows you to pay anybody else near-instantly for near-zero cost, doesn’t this mean Visa and Mastercard will soon be dead? My answer was no. If you believe all they do is payments then Bitcoin is a mortal threat… but that isn’t why they’re valuable. These networks are valuable to us because they promise universal acceptance – they minimize “acceptance anxiety”* no matter where we are in the world. And they have sophisticated rule-books: disputes and chargebacks give consumers and merchants certainty about what will happen when things go wrong. These things are valuable.

Third, I argued that – regardless of whether cryptocurrencies gain widespread adoption – they are already influencing today’s mainstream banking debates. Companies like XBTerminal have shown us how to route Bitcoin push-payment transactions via the terminal, to overcome the problem of mobile devices with no data connection. Peter Keenan, the Chief Executive of Zapp, was at the event and I pointed out how this approach could solve the problem his service will face when customers try to use it in underground shopping malls…

* An aside on “acceptance anxiety”: this is what I call the fear that your payment instrument won’t work when you try to use it. My prediction is that any retail payment solution has to induce less acceptance anxiety than existing methods if consumers are going to adopt it

By way of example, here’s my attempt at using a Bitcoin ATM in Shoreditch… my colleague’s smartphone wallet wasn’t working so I tried my laptop. This is not quite the seamless consumer experience we aspire to 🙂 (not yet…)

How are Banks supposed to formulate strategy when faced with a bewildering landcape of altcoins, sidechains, treechains and who knows what else?

Answer: by keeping laser-focussed on the principles – and ignoring everything else.

This is why I am so maniacal about hammering home phrases like:

- “Value transfer at a distance with no third party”

- “Internet-scale open platform for value exchange”

- “Solving the problem of coming to consensus with people you don’t know, don’t trust and where many of whom are trying to steal your money”

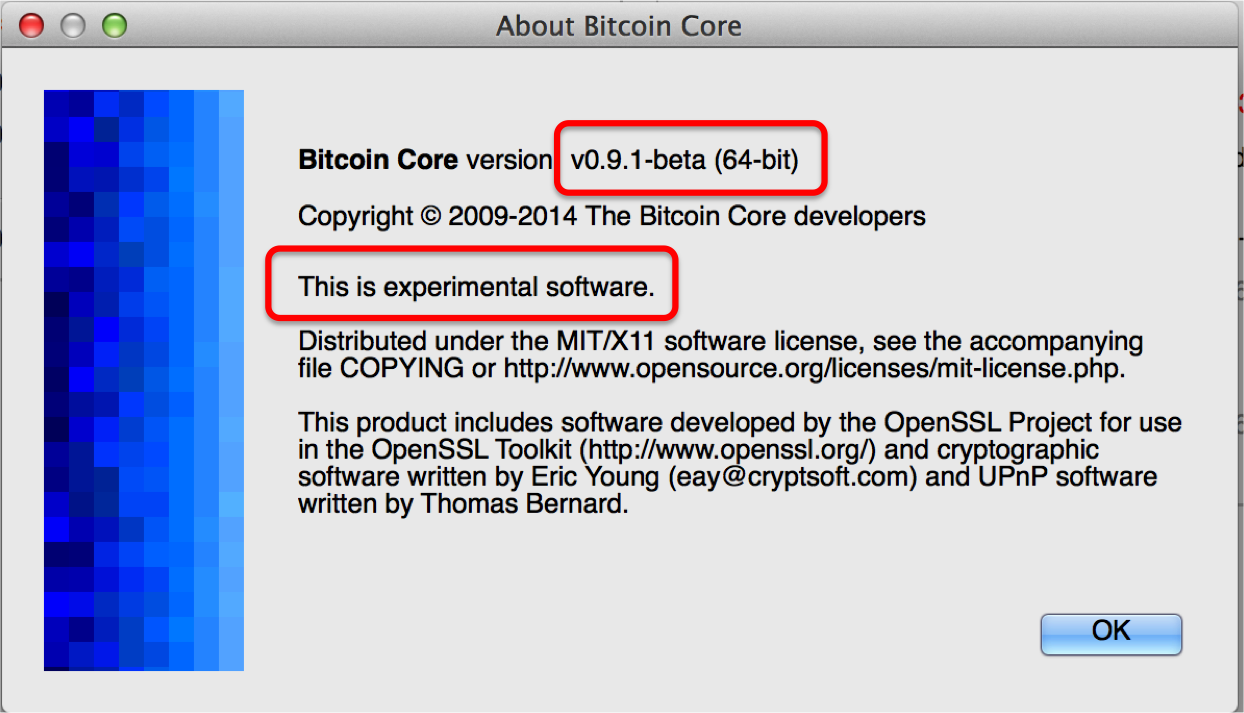

We have to keep focused on these principles because the reality is that the underlying technical details are constantly changing. It may not be obvious to outsiders but it’s important to realize that the cryptocurrency phenomenon is an experiment. Fire up a copy of Bitcoin Core and look at the “about” dialog. Here’s mine:

“This is experimental software”

This point is important: the Bitcoin we see today is not the Bitcoin we will be running in two years’ time. Many of today’s supposed problems (transaction throughput limitations, slow confirmation of transactions, …) will have been addressed through sidechains, treechains or solutions that haven’t even been invented yet.

So the only way to formulate strategy today is to keep focused on the principles and to ignore those details that are purely transient.

Ask yourself: what happens if our customers can send money instantly and for free? What happens if push-payments become universal? What happens if we can settle securities transactions, with finality, without needing clearing houses, custodians and CSDs? …

But banks should also bear in mind that widespread adoption could take longer than we expect:

Ask a technologist when the web went “mainstream” and they’ll probably say 1994 or 1995. But this answer is wrong by a decade! Facebook wasn’t even founded until 2004. Twitter? 2006. But even this misses the point. The transformational impact of the web (the internet-scale open platform for information exchange, remember…) was that it enabled the mobile and cloud revolutions. Yet Amazon Web Services didn’t launch until 2006 and the first iPhone wasn’t released until 2007.

And on top of this, the reality is that most mainstream users of cryptocurrency technology won’t even know they’re using it.

The only way to stay sane is to focus on the principles.

What about trust?

After the panel, I was approached by a member of the audience who was astonished that we hadn’t touched on the topic of trust. Fair point. Finextra’s Matt White was nearby and grabbed me for a two-minute follow-up:

My thanks to Elizabeth Lumley, Nick Hastings and the Finextra team for organizing such an excellent event.

[Updated 2014-05-05 with clearer Live-Scribe image]

Reblogged this on The Bitcoin Rat and commented:

Very Interesting and thoughtful piece from Richard Brown of IBM UK

The benefit to international money remittances is really bogus. The cost of international remittances lies with the cash in and cash out infrastructure and human beings at each end, not the moving of bits in between.

Until someone in the Ivory Coast can buy produce from the local market in bitcoins, transferring money to him/her from the US or Europe with the Bitcoin protocol achieves exactly nothing.

@Patrice – I share some of your scepticism and said so when I spoke. However, I’d highlight two points:

1) You don’t need local goods/services to be denominated in Bitcoin for this to work: it only needs to take cost out of the “transmission across borders” part of the problem.

2) Don’t assume the design of future remittance services will look like today’s. e.g. Kipochi’s had a service last year that allowed you to send them Bitcoin, which they would use to fund an m-pesa wallet… no need for a dedicated local agent network.

So – not as easy as some make it sound… but I think of it as an enabler to enhanced productivity in this space… not the entire answer

I’m not sure how long the bubble can last, which is why I only trade with arbitrage. Freestaking.com helps with that alot