The retail use-cases get all the press… but the killer-app for digital central bank money might be smart contracts

This post on a concept called “FedCoin” by David Andolfatto of the St Louis Fed raises the really interesting possibility of a world with central-bank-issued digital assets which can be held by a broad range of people.

Andolfatto’s FedCoin post

The core idea is essentially a variation on the digital cash theme: a digital bearer asset that is redeemable for dollars. So, on the surface, just like m-pesa but for dollars, right?

Not quite. Because Andolfatto’s FedCoin idea has two important differences.

- First, FedCoin would be issued by the central bank. That contrasts with most other digital cash systems, where the holder has a claim against a telecoms firm or a commercial bank. In those systems, you have to trust the central bank not to inflate away the currency (as you do here) but you also have to trust the commercial issuer not to go bust – or any deposit insurance scheme to bail you out if they do. A central bank digital asset doesn’t have that second issue.

- Secondly, Aldolfatto suggests this currency could be issued on a distributed ledger. As he writes in an update to that post, many people have questioned why that might be necessary. Surely if you trust the fed enough to hold its currency, you trust it to run an accounting system! However, I wouldn’t dismiss this suggestion just yet, as I’ll argue below.

Robert Sams has an intelligent and thoughtful analysis of the overall idea.

So why am I writing about it now?

It’s not just the US: what about the Bank of England?

No sooner had the FedCoin idea been discussed and dissected, the Bank of England published its 2015 “Research Agenda”: a paper summarizing all the questions they plan to examine this year.

Turn to page 31 and guess what… there’s a section on Digital Currencies. If you haven’t read it, I urge you to do so. Because it doesn’t say what one might expect it to. Most official papers on “digital currencies” are influenced by Bitcoin and talk about volatility, monetary questions, the tedious question of whether cryptocurrencies pass the “money test”, regulation and so forth.

This paper doesn’t. Instead, it follows the same line of reasoning as Andolfatto and focuses directly on the question of what a central bank-issued digital currency might mean. And the paper does something really valuable: it lists a set of questions that anybody planning to do something in this space would have to answer.

The Bank of England’s Research Questions for a Central-Bank-issued digital currency

And these are important questions. Imagine something like FedCoin was built and you were able to hold a digital asset that represented a claim on the Bank of England or the Federal Reserve. The implications for commercial banks could be huge: why would you lend your money to (aka “deposit with”) a retail bank if you could hold the same money in a counterparty-risk-free form?

So the commercial banks would probably have to compete for your deposits with higher interest rates. But wouldn’t that make them more risky and more likely to fail? So perhaps the central bank would have to charge you to hold their digital asset (a negative interest rate?) to encourage you not to hold too much of it and lend the rest to the commercial banks. But now the digital “cash” isn’t the same as physical cash…

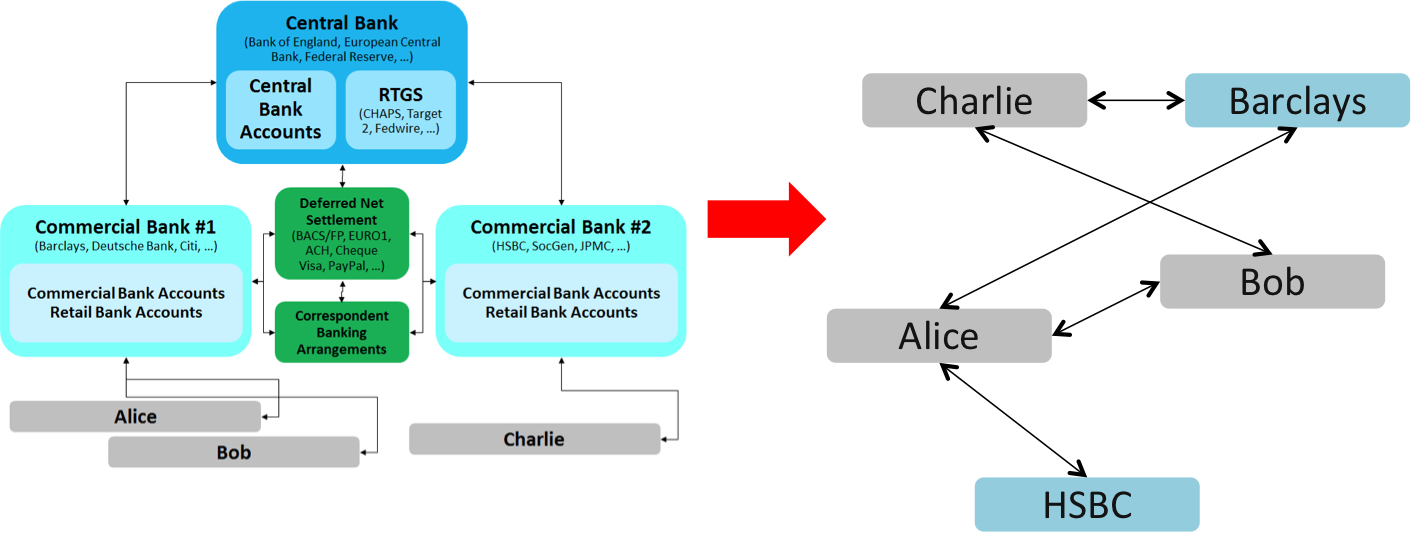

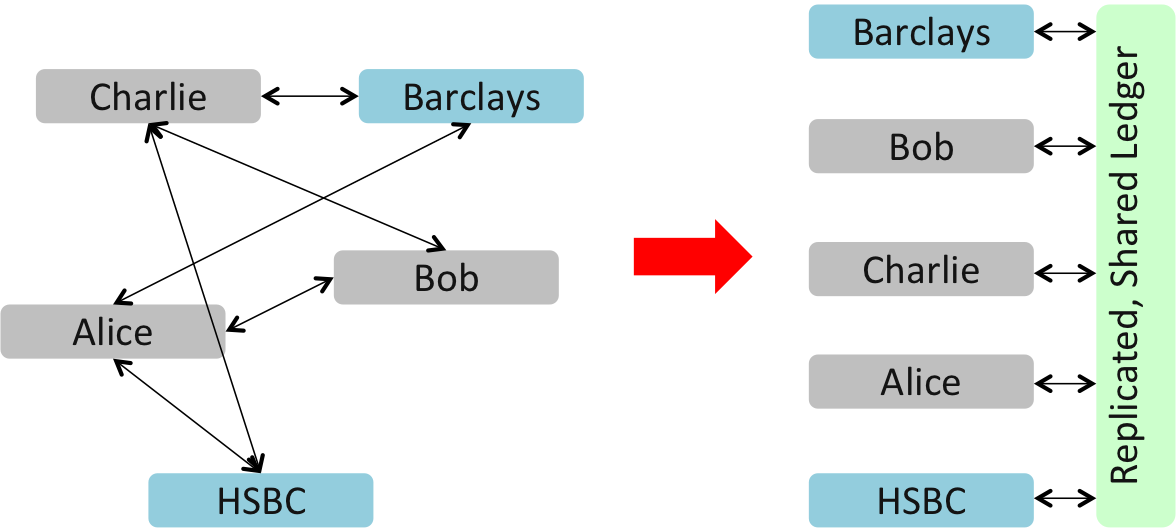

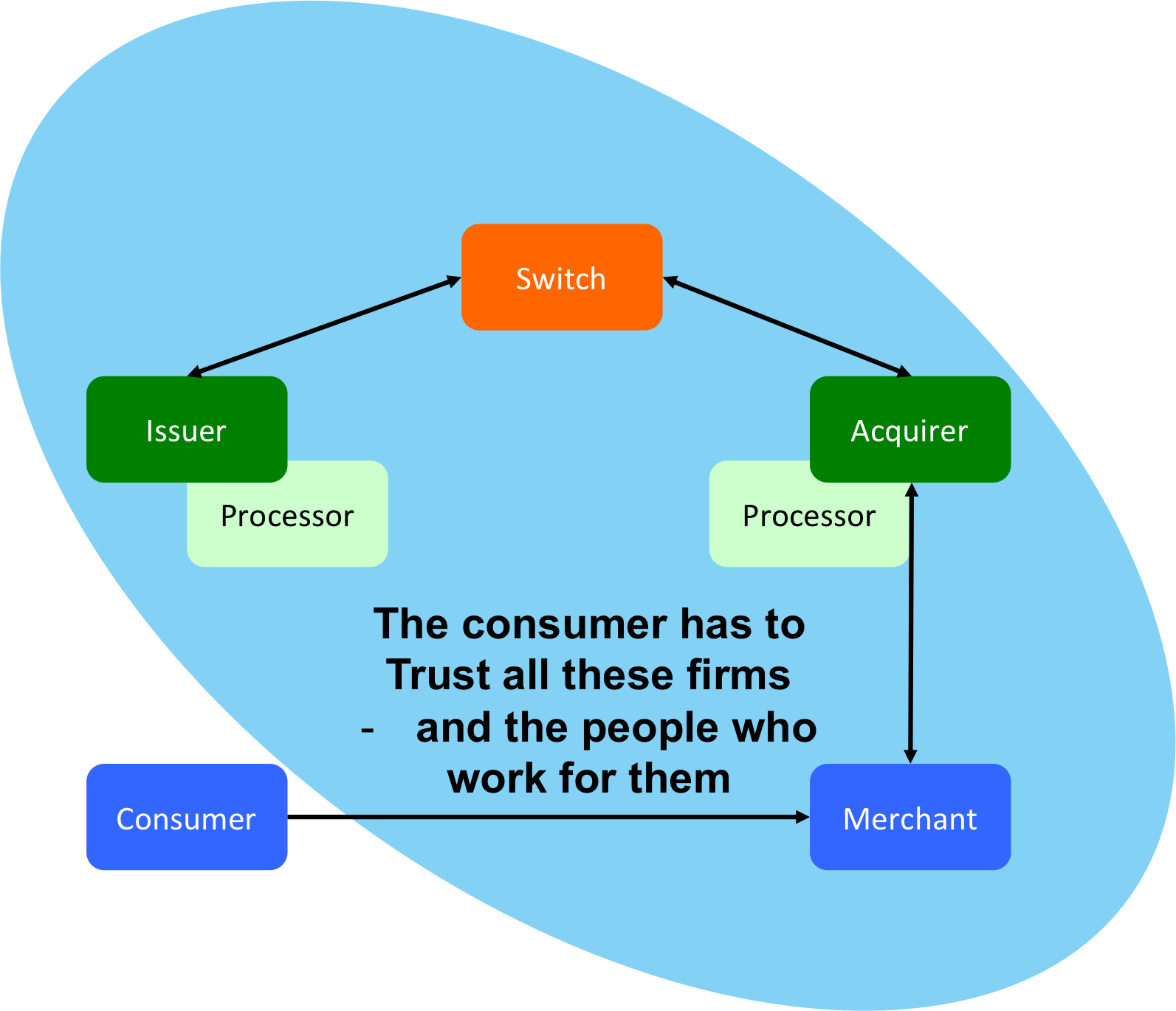

And there’s another question. If everybody has access to central bank money, then why do we need payment systems? I wrote a simplified explanation of how money moves around the banking system a while back – and the noteworthy thing about it is that pretty much all of the payment infrastructure in the world exists because most money isn’t central bank money. If you imagine a world where everybody holds central bank money, suddenly the picture begins to look a lot simpler…

Do you need need most payment systems in a world with only FedCoin…?

There’s more… Do we really want people having access to unlimited amounts of digital bearer assets denominated in GBP or USD? Do central banks have the culture, systems and experience to oversee such a scheme and spot misuse, fraud and crime?

So perhaps a hybrid implementation, would emerge where consumers have to nominate a “sponsoring” commercial bank, which provides safekeeping services, has oversight responsibilities and, perhaps, has the ability to block suspicious transactions?

Who knows. And I should stress that I don’t think anybody is proposing a system like this in any case…. These are research questions. But it suggests that the BOE questions are a very good starting point for thinking about these issues.

A solution looking for a problem?

But there’s a small issue: this intellectual exercise is fascinating but is a central bank digital currency actually needed? With a few notable exceptions, depositors don’t tend to lose their deposits when commercial banks fail. (But businesses and other large depositors often do…) And aren’t capital rules and prudential supervision designed to solve that problem in any case?

Remember I said the “distributed ledger” aspect of FedCoin was interesting…

Think back to the Andolfatto piece. He mused about building “FedCoin” on a distributed ledger. On its face, that doesn’t seem to make much sense.

But if we open the topic of distributed ledgers, it also brings Smart Contracts into play. In my recent piece on the topic, I suggested a definition for a smart contract as follows:

“A smart-contract is an event-driven program, with state, which runs on a replicated, shared ledger and which can take custody over assets on that ledger.”

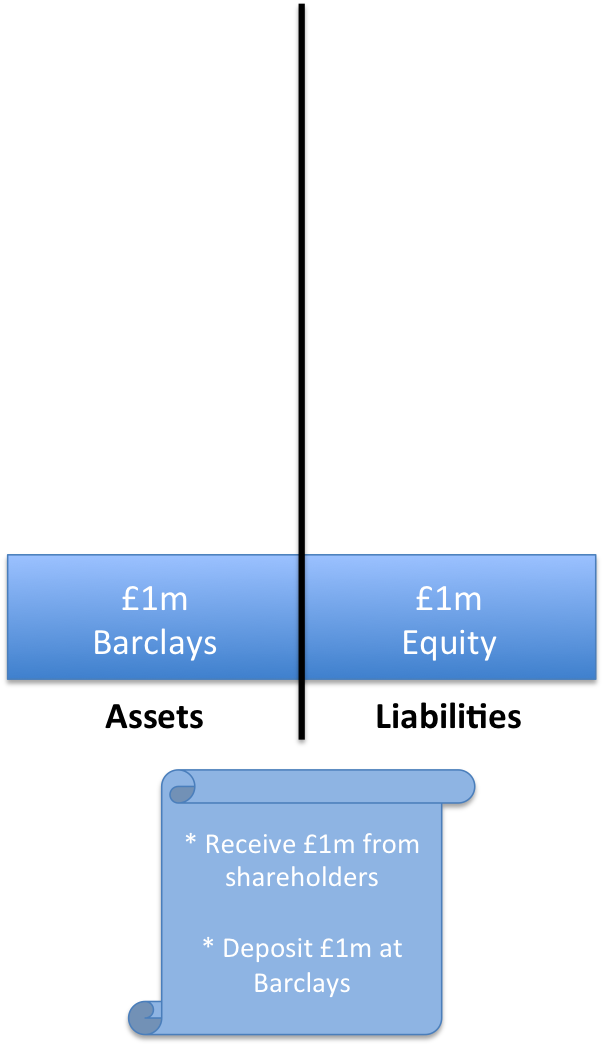

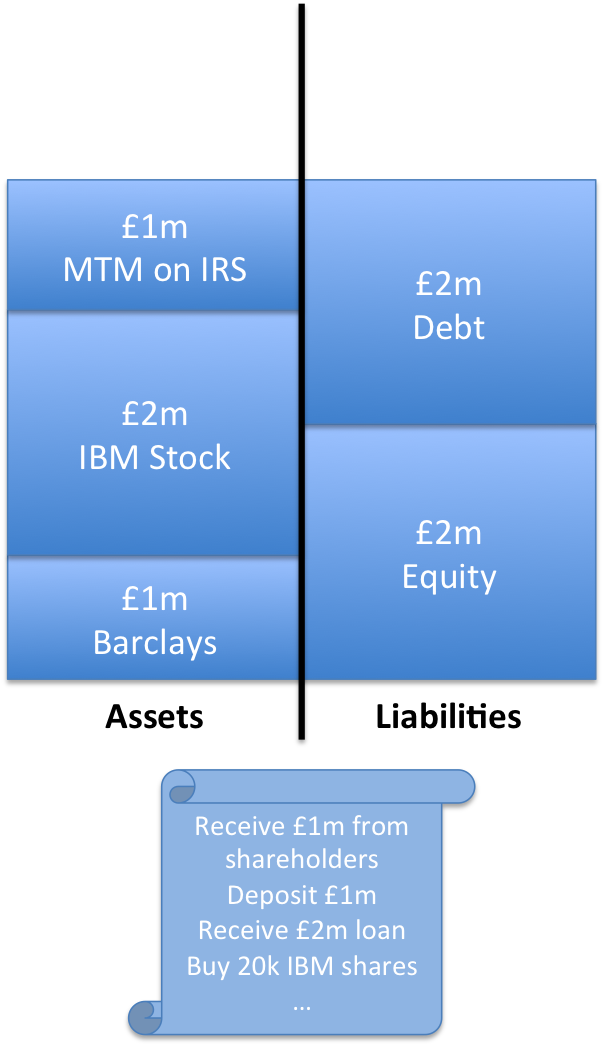

Implicit in my definition was that these “assets” could be native assets to the ledger (e.g. Bitcoin). But , more likely, they would be representations of real-world assets: GBP tokens issued by Barclays or HSBC or Coop, say.

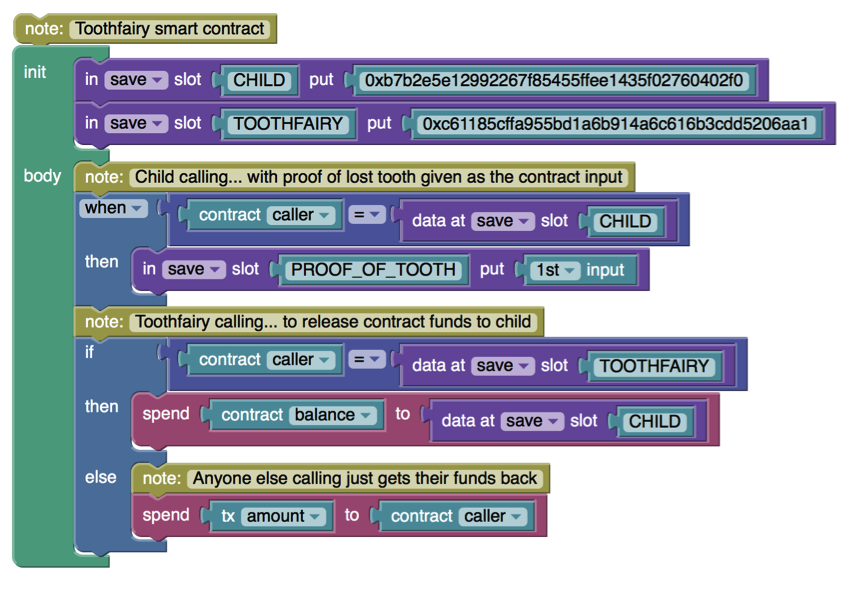

For example, you could imagine consumers paying £50 a month into a “mobile phone insurance smart contract” and, if they can provide proof that they’ve lost their mobile phone, the smart contract will pay out enough money to replace the phone, using the funds that have been paid in by all the policyholders.

Perhaps the “proof” would be in the form of a “proof of purchase”, signed by a retailer and an “attestation of loss”, cosigned by the policy holder and a police officer. The details here don’t matter too much.

But what does matter is the payment.

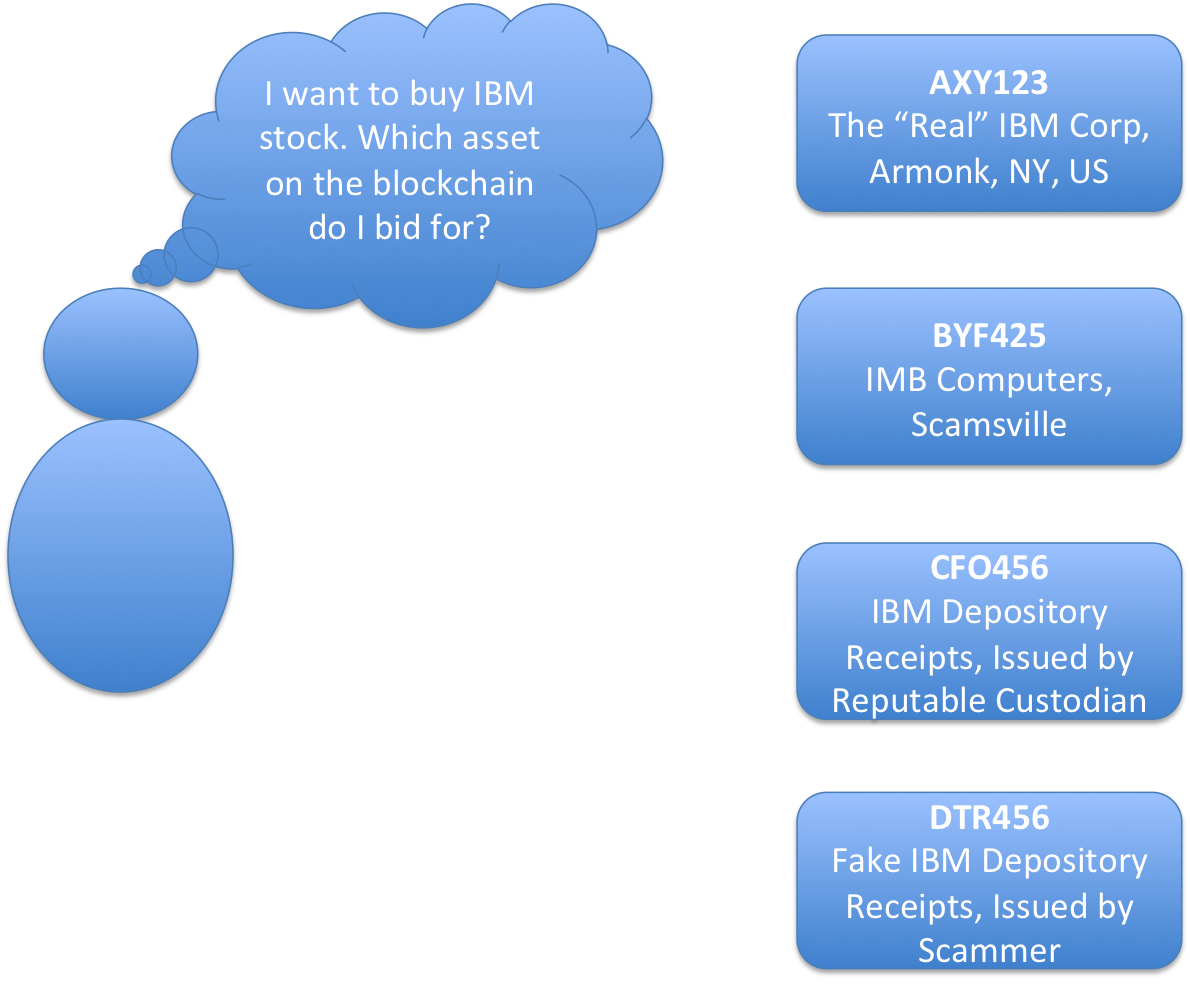

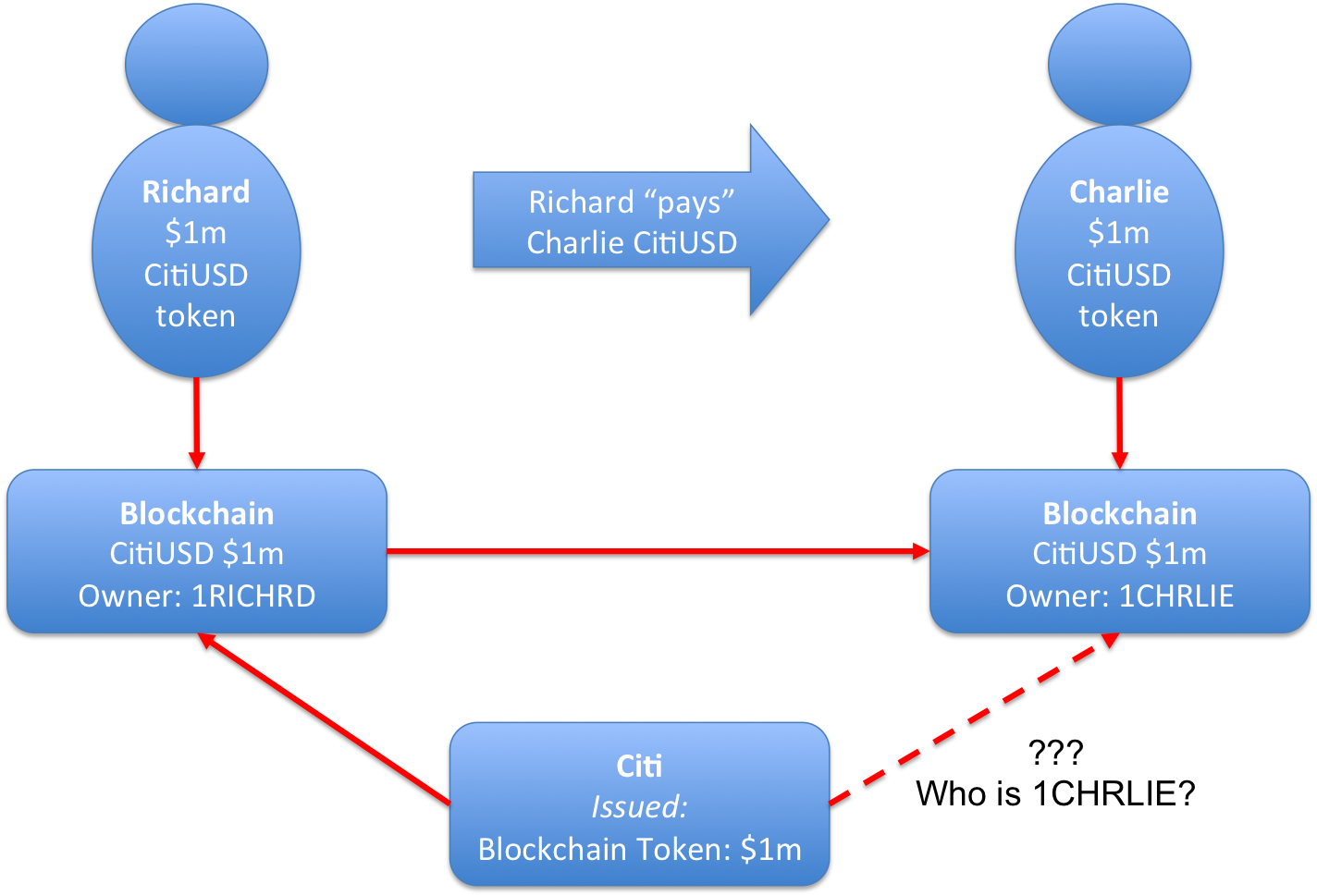

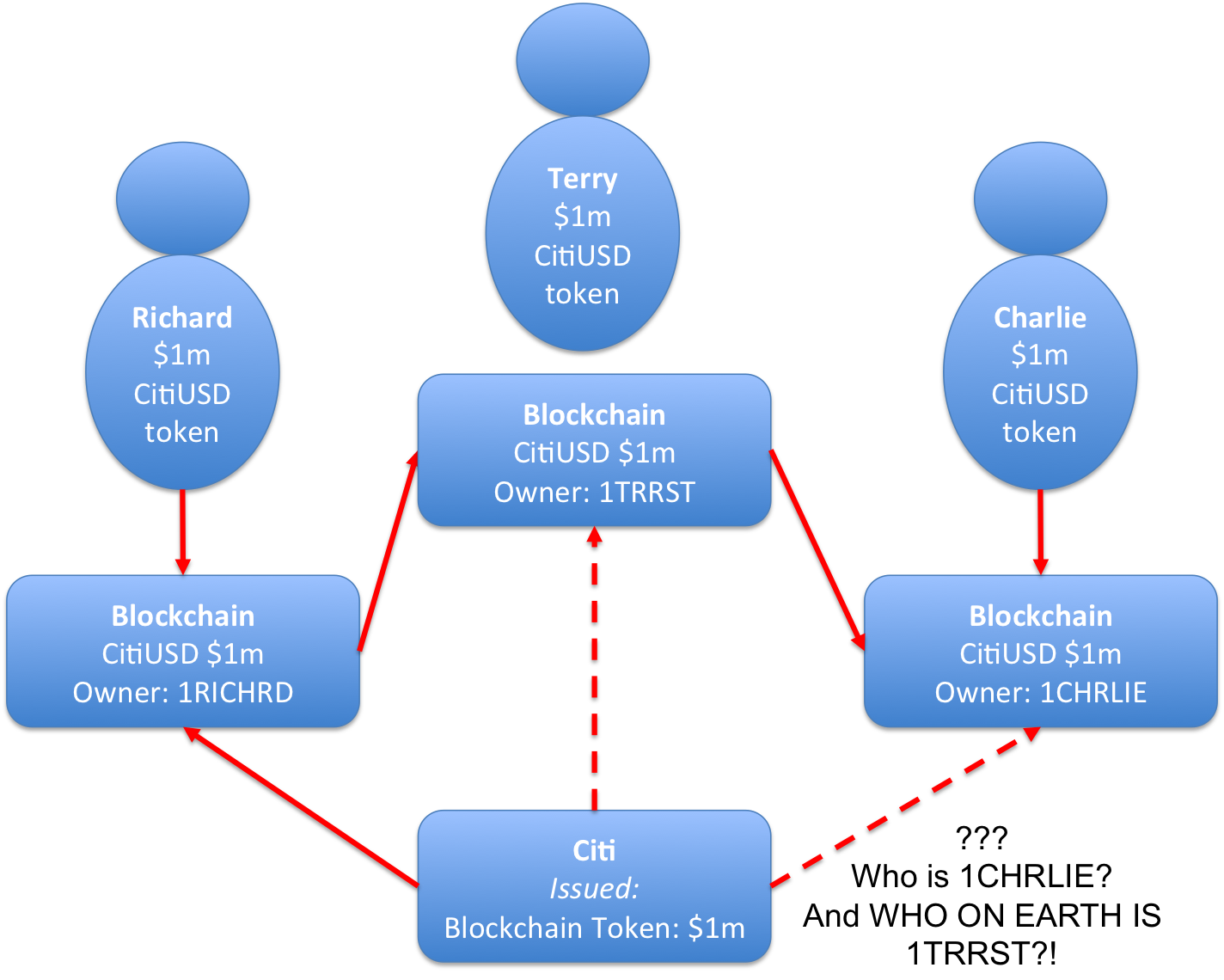

How would you write a contract like this so that it could be sold to as many consumers as possible? They probably have accounts with different banks and, if we imagine a world of distributed ledgers, they’d all be holding different tokens: GBP-Barclays, GBP-Coop and so on.

Which tokens should an insurance contract accept from its customers? Only tokens issued by “safe” banks? Which ones? Who controls the list? What about a £1000 IOU from me? Would the smart contract accept that? What about a £1000 IOU from a billionaire?

What happens when the contract pays out? If you had paid in GBP-Barclays, how would you feel about receiving an arbitrary mix of GBP assets when you made a claim, based on whatever happened to be in the pool at the time?

Writing a smart contract that deals with GBP issued by multiple issuers gets complicated very quickly…

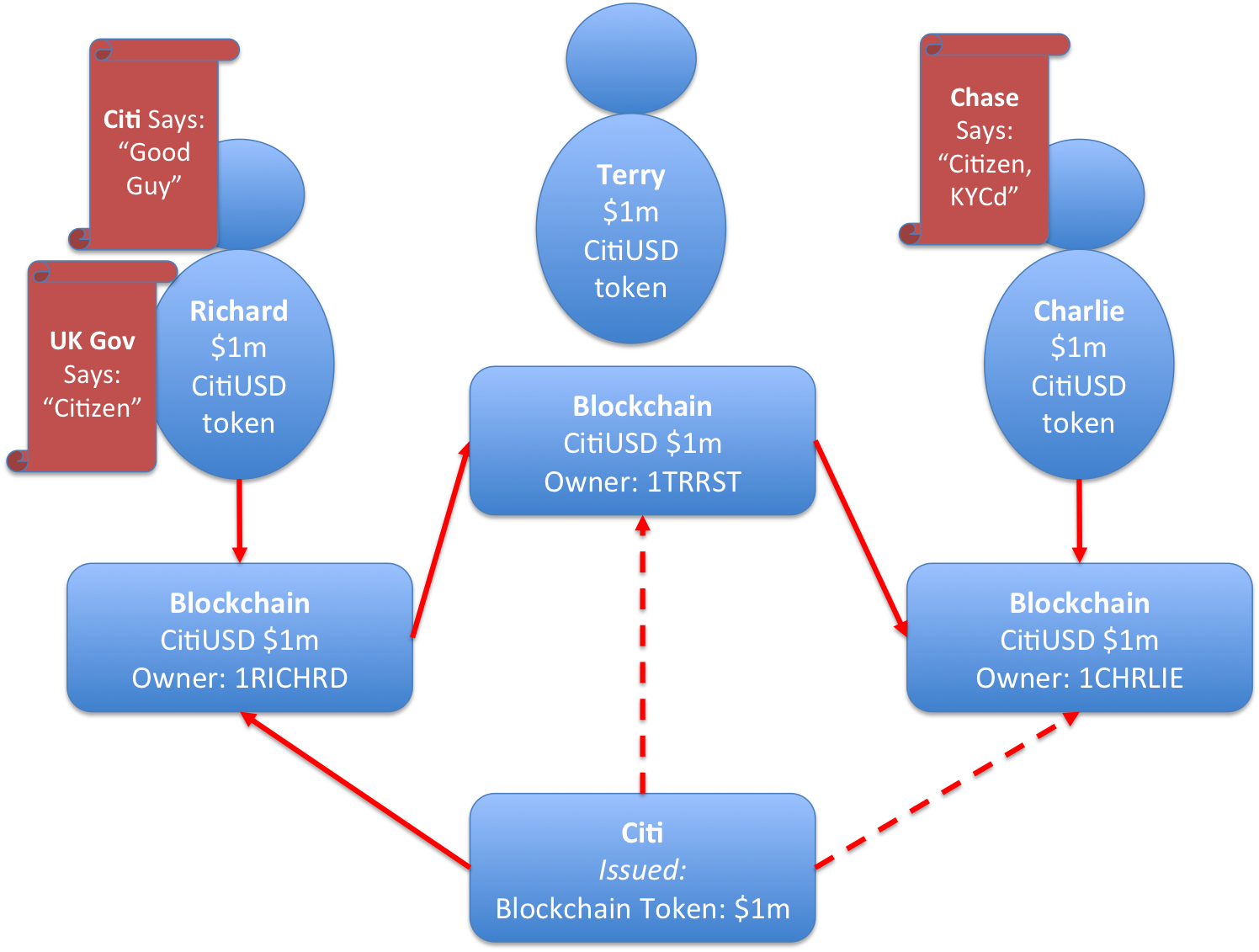

Systems like Ripple solve this problem by explicitly modeling the idea of an asset and its issuer. 50 GBP-Barclays is different to 50 GBP-HSBC and Ripple is built on that insight. So you could certainly configure the contract to trust some issuers but not others.

But it gets complicated. What happens if one of those issuers gets taken over? Goes bust? Who updates the list of “trusted” issuers in the smart contract?

And now, scale the problem up to the institutional side of the world, where the sums involved in derivatives contracts are enormous. Suddenly the identity of the issuer really matters.

And this is where I think a central bank digital currency could make sense on a distributed ledger. It would clear away all that complexity.

You could simply write the contract to demand payment in the central bank token. Policyholders would have the responsibility of converting other GBP assets into the central bank issued asset.

Now, perhaps this wouldn’t be a problem in real life – maybe you could just write the smart contract to only accept GBP-Barclays, say, and insist customers of other banks convert into Barclays tokens in order to use the contract. But having a counterparty-risk-free representation of fiat currencies on these smart contract systems feels like it could be extremely useful.

But time will tell, as always.